Tamilnadu State Board New Syllabus Samacheer Kalvi 12th Commerce Guide Pdf Chapter 28 Company Secretary Text Book Back Questions and Answers, Notes.

Tamilnadu Samacheer Kalvi 12th Commerce Solutions Chapter 28 Company Secretary

12th Commerce Guide Company Secretary Text Book Back Questions and Answers

I. Choose the Correct Answers

Question 1.

Mention the status of a Company Secretary in a company.

a) A member

b) A director

c) An independent contractor

d) An employee contractor

Answer:

d) An employee contractor

Question 2.

Who can become a secretary for a company?

a) Individual person

b) Partnership firm

c) Co-operative societies

d) Trade unions

Answer:

a) Individual person

![]()

Question 3.

Which meeting will be held only once in the life time of the company?

a) Statutory

b) Annual General .

c) Extra – ordinary

d) Class General

Answer:

a) Statutory

Question 4.

Board Meetings to be conducted minimum ________ times in a year.

a) 2

b) 3

c) 4

d) 5

Answer:

c) 4

![]()

Question 5.

Who is not entitled to speak at the annual general meeting of the company.

a) Auditor

b) Shareholder

c) Proxy

d) Directors

Answer:

c) Proxy

Question 6.

Mention the company which need not convene the Statutory Meeting.

a) Widely held public

b) Private Limited

c) Public Limited

d) Guarantee having a share capital

Answer:

b) Private Limited

![]()

Question 7.

From the date of its incorporation the First Annual General Meeting is to be conducted

with in …………….. months.

a) Twelve

b) Fifteen

c) Eighteen

d) Twenty one

Answer:

c) Eighteen

Question 8.

What percentage of shareholders is needed to pass special resolution?

a) It must be unanimous

b) Not less than 90%

c) Not less than 75%

d) More than 50%

Answer:

c) Not less than 75%

Question 9.

A special resolution must be filed with the Registrar within

a) 7 days

b) 14 days

c) 30 days

d) 60 days

Answer:

c) 30 days

![]()

Question 10.

A special resolution is required to .

a) redeem the debentures

b) declare dividend

c) appoint directors

d) appoint auditor

Answer:

d) appoint auditor

II. Very Short Answer Questions

Question 1.

Who is a Secretary?

Answer

The person who is responsible for the general performance of an organization is called the company secretary.

Question 2.

What is meant by Meeting?

Answer:

A meeting is a gathering of two or more person that has been convened for the purpose of achieving a common goal through verbal interaction such as sharing information or reaching agreement.

Question 3.

What is Resolution?

Answer:

As per the Companies Act 2013, for taking any decision or executing any transaction, the consent of the shareholders, the Board of Directors and other specified is required. The decisions taken at a meeting are called resolutions

![]()

Question 4.

Write a Short note on ‘Proxy’.

Answer:

- “Proxy” means a person is the representative of a shareholder at the meeting of the

- He may be described as the agent of a shareholder to carry out which he has himself decide upon.

- He can be present at the meeting and vote but cannot talk.

Question 5.

What is Vote?

Answer:

The word ‘Vote’ originated from Latin word ‘Votum’ indicating one’s wishes or desire. By casting his vote one formally declares his opinion or wish in favour of or against a proposal or a candidate to be elected for an office.

III. Short Answer Questions

Question 1.

What is Special Resolution?

Answer:

- “Special Resolution” is one which is passed by not less than 75% of majority. [3/4th majority]

- The number of votes cast in favour of the resolution should be three times the number of votes cast against it.

![]()

Question 2.

What do you mean by Statutory Meeting?

Answer:

- The First Meeting of the Company.

- This is convened only once in the life time of the company.

- It should hold the meeting of shareholders with in 6 months but not earlier than one month from the date of commencement of business of the company.

Question 3.

Give any three cases in which an ordinary resolution need to be passed.

Answer:

- To change the name of a company.

- To alter the share capital.

- To redeem debentures.

- To declare dividends.

- To approve annual accounts and Balance Sheet.

- To appoint the Directors.

Question 4.

What resolution requires special notice?

- There are certain matters specified in the Companies Act 2013, which may be discussed at General Meeting only if a special notice is given at least 14 days before the meeting.

- The following matters require special notice.

- To remove the director before the expiry of his period.

- To appoint a director in the place of a director so removed.

- To reappoint the retiring Auditor.

![]()

IV. Long Answer Questions

Question 1.

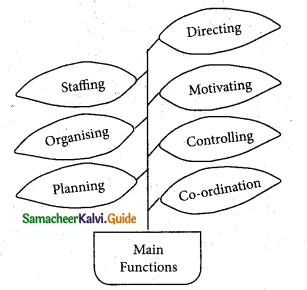

Elaborate the Functions of the company secretary.

Answer:

The functions of the Company Secretary may be divided into two types. They are:

- Statutory functions

- Non-Statutory functions

Statutory Functions: As the principal officer of the company, the secretary must observe all the legal formalities in respect of the provisions of the Companies Act and other laws, for the activities of the company.

According to Companies Act 2013:

- To sign document and proceedings requiring authentication by the company

- To maintain share registers and register of directors and of contracts.

- TO give notice to register for increase in the share capital

- To send notice of general meeting to every member of the company

- To prepare minutes of every general meeting and board meeting within 30 days

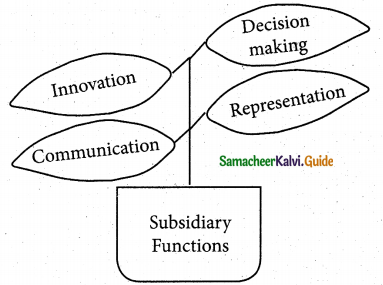

Non-Statutory Functions: The secretary has to discharge non-statutory functions in relation to directors, shareholders and office and staff.

Functions in Relation to Directors: A company secretary acts under the full control of the board of directors and carry out the instructions of the directors.

The secretary will arrange board meetings issuing notice, and preparing agenda of meetings, recording the attendance and minutes of meetings.

Functions in Relation to Shareholders: The company secretary must serve in the best interests of the shareholders.

He has to arrange the issue of allotment letters, call letters, letters of regret, share certificates, and share warrants to Shareholders.

Functions in Relation to Office and Staff: The secretary is responsible for the smooth functioning of the office work. He exercises overall supervision, control and co-ordination of all clerical activities in the office.

![]()

Question 2.

Briefly state different types of Company Meetings.

Answer:

I. Meeting of Shareholders :

a. Statuary Meeting.

b. Annual General Meeting.

c. Extra Ordinary [Special] General Meeting.

II. Meetings of Directors :

a. Board Meeting.

b. Committee Meeting.

III. Special Meetings:

a. Class Meeting.

b. Creditors Meeting.

I) Meetings of Shareholders :

a) Statutory Meeting:

- The First Meeting of the Company.

- This is convened only once in the life time of the company.

- It should hold the meeting of shareholder within 6 months but not earlier than 1 month from the date of commencement of business of the company.

b) Annual General Meeting:

- Usually it is convened once in a year.

- The first AGM convened within 18 months from the date of Registration.

- The time gap between two consecutive AGM should not exceed 15 months.

- It should be convened where the Registered office situated or in any other place.

- Every AGM shall be held during business hours, on a day which is not a public holiday.

c) Extra-Ordinary [Special] General Meeting:

- All other General Meetings other than Statutory Meeting and AGM are called “Extra – Ordinary [Special] General Meeting”.

- If any meeting convened in between two AGM to deal with some urgent or special nature it is called Extra Ordinary General Meeting.

II) Meetings of Directors :

a) Board Meeting:

- Meetings of the Directors are called “Board Meeting”.

- The First Board Meeting should be convened with in 30 days from the date of incorporation of the company.

- It should be conducted at least 4 times in a year. [Once in 3 months]

b) Committee Meeting:

- The Committee [Audit] meet at least four times in a year. [Listed Companies or public limited company having share capital of ₹ 10 crores or more]

- If the share capital less than ₹ 10 crores, a Director should be appointed by the Board to the “Audit Committee”.

III) Special Meeting:

a) Class Meeting:

- Meetings, which are held by a particular class of (preference shareholder or Debenture holder) is known as class meeting.

b) Meeting of the Creditor:

- These are not the meetings of the company.

- A situation in which a company may with to arrive at a consensues with the creditor to avoid any crisis or to evolve compromise or to introduce any new proposals.

![]()

Question 3.

Explain different Types of Open and Secret Types of Voting.

Answer:

I) Open Procedure:

a) By Voice:

- Voice voting in which the chairman allows the members to raise their voice in favour or against an issue.

“Yes” for Approval

“No” for Rejection. - The chairman announces the results of voice voting on the basis of strength of words shouted.

b) By Show of Hands :

- Under this method, the chairman requests the members to raise their hands of those who are in favour of the proposal or candidate and then requests those are against.

- He announces the result on the basis of hands counted.

II) Secret Procedure:

a) By Ballot:

- Under this method, Ballot Paper Bearing Serial Number a (Symbol) is given to the members to record their opinion by marking with a symbol [S], they have to cast their vote in a secret chamber and put the ballot paper into the ballot box.

- The votes are counted and the results are announced.

b) By Post [Postal Ballot]:

- Big Companies or Big Associations having members scattered all over the country follow this method of voting.

- The members or voters fill in the ballot papers and return them by post in sealed covers which are opened when the ballot box is opened for counting the votes.

c) By Electronic Voting Machine [EVM]:

- It is a new technique of voting.

- Instead of using Ballot paper this machine is used.

- Names and symbols are fixed in the machine.

- The voter has to press the button.

- If green light signal comes it is in favour.

- If red light signal comes it is unfavour.

![]()

12th Commerce Guide Company Secretary Additional Important Questions and Answers

I. Choose the Correct Answers

Question 1.

A statutory meeting can be held within _________ months.

(a) 10

(b) 5

(c) 6

(d) 3

Answer:

(c) 6

Question 2.

The Latin word ‘Secretariats’ means …………….

a) Secret

b) Open

c) Delegate

d) complete

Answer:

a) Secret

![]()

Question 3.

An ordinary resolution is one which can be passed by a _________ majority.

(a) simple

(b) special

(c) high

(d) low

Answer:

(a) simple

Question 4.

A notice must be sent to every member to attend meeting …………………. days before the meeting is to be held. .

a) 7

b) 14

c) 21

d) 28

Answer:

c) 21

![]()

Question 5.

……………. means a person being the representative of a shareholder to attend a meeting on behalf of him.

a) Proxy

b) Substitute

c) Alternate

d) NOTA

Answer:

a) Proxy

Question 6.

Requisite number of persons at the meeting is called ……………….

a) Quorum

b) Proxy

c) Vote

d) Poll

Answer:

a) Quorum

Question 7.

Quorum for private limited company is ………………….

a) 1

b) 2

c) 3

d) 4

Answer:

b) 2

![]()

Question 8.

Quorum for public limited company is …………………

a) 3

b) 4

c) 5

d) 6

Answer:

c) 5

Question 9.

Which meeting will be held only once in the lifetime of the company?

a) AGM

b) Class

c) Board

d) Statutory

Answer:

d) Statutory

Question 10.

A Company Secretary is appointed by …………….

a) Government

b) Institute of Company Secretary

c) Board of Directors

d) Shareholders

Answer:

c) Board of Directors

![]()

Question 11.

Statutory meeting hold within …………….. months but not earlier than …………….. month.

a) 6 and 1

b) 6 and 2

c) 1 and 6

d) 6 and 3

Answer:

a) 6 and 1

Question 12.

The AGM convened within …………….. months.

a) 15

b) 18

c) 21

d) 25

Answer:

b) 18

Question 13.

The time gap between two consecutive AGM is ……………… months.

a) 3

b) 6

c) 12

d) 15

Answer:

d) 15

![]()

Question 14.

Director is Acting as ………………….

a) Agent

b) Trustee

c) Officer

d) All of these

Answer:

d) All of these

Question 15.

Who can call Extraordinary General Meeting?

a) CLT

b) Board

c) Requisition, Requisitioriists

d) All of these

Answer:

d) All of these

Question 16.

The decisions taken at a meeting are called ………………

a) Resolution

b) Poll

c) Vote

d) NOTA

Answer:

a) Resolution

![]()

Question 17.

……………….. resolution is one can be passed by a simple majority.

a) Ordinary

b) Special

c) Requiring Special Notice

d) All of these

Answer:

a) Ordinary

Question 18.

……………….. resolution is one can be passed by three fourth majority.

a) Ordinary

b) Special

c) Requiring Special Notice

d) All of these

Answer:

b) Special

Question 19.

The word vote is derived from the Latin word ………….

a) Votum

b) Voter

c) Voted

d) NOTA

Answer:

a) Votum

![]()

Question 20.

An authenticated record of a meeting is known as ………………

a) Agenda

b) Minutes

c) Ledger

d) NOTA

Answer:

b) Minutes

Question 21.

Pick the odd one out:

a) By Ballot

b) By Postal Ballot

c) By EVM

d) By Voice

Answer:

b) By Voice

Question 22.

Pick the odd one out:

a) Statutory Meeting

b) ACM

c) Extra-Ordinary General Meeting

d) Class Meeting

Answer:

d) Class Meeting

![]()

Question 23.

Which one of the following not correctly matched?

a) Statutory Meeting – Statutory Report

b) AGM – To appoint directors

c) Class Meeting – Preference shareholders meeting

d) Committee Meeting – Shareholders meeting

Answer:

d) Committee Meeting – Shareholders meeting

Question 24.

Choose the correct statement.

i) Proxy is a person who participates in the meeting on behalf of a shareholder.

ii) He can attend and vote in the meeting.

iii) He cannot speak in the meeting.

a) (i) is correct

b) (ii) is correct

c) (iii) is correct

d) (i), (ii) and (iii) are correct

Answer:

d) (i), (ii) and (iii) are correct

![]()

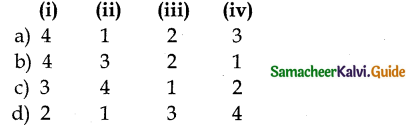

II Match the following.

Question 1.

| List – I | List – II |

| i. Agenda | 1. Record of the proceedings of the meeting |

| ii. Minutes | 2. Minimum number of members necessary for a meeting |

| iii . Quorum | 3. A person appointed to attend and vote at the meeting |

| iv. Proxy | 4. Order of events to be held in the meeting |

Answer:

a) (i) 4, (11) 1, (iii) 2, (iv) 3

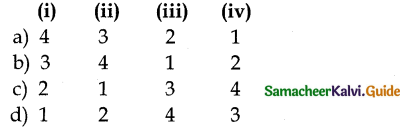

Question 2.

| List – I | List – II |

| i. Ordinary Resolution | 1. To appoint the retiring Auditor |

| ii. Special Resolution | 2. Proposal placed before a meeting |

| iii.. Requiring Special notice | 3. Support by a simple majority |

| iv. Motion | 4. Support by three fourth majority |

Answer:

b) (i) 3, (n) 4, (iii) 1, (iv) 2

![]()

III. Assertion and Reason

Question 1.

Assertion (A): Special Resolution is passed by three fourth majority.

Reason (R): The number of votes cast in favour of the resolution should be three times, the number of votes cast against it.

a) (A) and (R) are True. (R) is the correct explanation of (A)

b) (A) and (R) are True. (R) is not the correct explanation of (A)

c) (A) is True (R) is False

d) (A) is False (R) is True

Answer:

a) (A) and (R) are True. (R) is the correct explanation of (A)

Question 2.

Assertion (A): Voice Voting in which the Chairman allows the members to raise their voice in favour or against an issue.

Reason (R): The chairman announces the results of voice voting on the basis of the strength of words shouted.

a) (A) and (R) are True. (R) is not the correct explanation of (A).

b) (A) and (R) are True. (R) is the correct explanation of (A).

c) (A) and (R) are False.

d) (A) is False (R) is True

Answer:

b) (A) and (R) are True. (R) is the correct explanation of (A)

![]()

IV. Very Short Answer Questions

Question 1.

Define Company Secretary.

Answer:

“Secretary means any individual possessing the prescribed qualifications, appointed to perform the duties which may be performed by a secretary under this Act and any other ministry or administrative duties”.

– Companies Act, 2013, Section 2 (24)

Question 2.

What do you understand by “Poll”?

Answer:

- Poll means tendering or offering a vote by ballot to a specially appointed officer, called the polling officer.

- Under the Companies Act, poll means exercising the voting right in the proportion to shareholders contributions the paid-up capital of a limited company having a share capital.

V. Long Answer Questions

Question 1.

What are the Qualifications of a Company Secretary?

Answer:

Statutory Qualifications:

- ACS – [Having Share Capital 5 crore or more] [Associates of the company secretary ship]

- B.L – Degree

- C.A. – [Member of Institute of Chartered Accountant]

- M.Com – Degree

- I.C.W.A – [Member of Institute of Cost and Works Accountant]

Other Qualifications:

- Thorough in Companies Act.

- Expertise in Business Laws.

- Know the Economic Laws.

- Having more knowledge of Accounting.

- Expertise in Labour Laws.

- Knowledge in Company Management and HRM.

![]()

Question 2.

How the company secretary is appointed?

Answer:

As per section 2 (247, 203, 204) of the companies Act 2013, the provisions are given for the appointment of the company secretary. Only an individual who is a member of the Institute of Company Secretaries of India can be „ appointed as a company secretary. There are two methods of appointment of the company secretary. They are given below:

- By the Promoters: The first secretary of a company is appointed by the promoters at the pre-incorporation stage.

- By the First board of Directors: After the company has been registered, the first board of directors appoints the secretary at the first board meeting.

Question 3.

What are the powers and Rights of the Company Secretary?

Answer:

- Excercising Power : He has the right to exercise powers as granted by Board.

- Claiming Salary : As per contract, he has the right to claim his salary and other allowances.

- Preferential Creditor : During winding up of a company, he can claim his legal dues on a preferential basis.

- Attending Meeting : He has the right to be physically present in the meeting of shareholders and Directors.

- Supervision and Control : As a head, he has a right to supervise, direct and control all office activities of the subordinates.

- Signing authority : Being a principal officer he can sign contracts

![]()

Question 4.

Discuss the Liabilities of Company Secretary.

Answer:

I. Statutory Liabilities:

- Register all files and documents of the company.

- Arrange AGM in due time.

- Sending notice of meeting to all the participants.

- Maintaining Minute Books.

- Issuing share certificate, share warrant to the shareholders.

II. Contractual Liabilities:

- Abide by all terms and conditions of service contract.

- Act as per the directions of Board.

- Maintain secretary of the company affairs.

- Perform duties with due care and skills.

- Never act beyond his authority.

- Not to earn secret profit through illegal activity.

Question 5.

Describe the different types of Resolutions which company may pass with suitable matters required for each type of resolution.

Answer:

Ordinary Resolution:

- An ordinary resolution is one which can be passed by a simple majority. [Not less than 51 %]

- The votes cast in favour of resolution is more than the votes cast against the resolution.

Ordinary Resolution is required for the following matters :

- To change the name of a company.

- To alter the share capital.

- To redeem debentures.

- To declare dividends.

- To approve annual accounts and Balance Sheet.

- To appoint the directors.

Special Resolution:

- “Special Resolution” is one which is passed by not less than 75% of majority. [3/4th majority]

- The number of votes cast in favour of the resolution should be three times the number of votes cast against it.

Special Resolution is required for the following matters:

- To change the Registered office from one state to another.

- To change the objectives of the company.

- To alter the AOA.

- To commence any new business.

- To appoint auditor.

Resolution requiring special notice :

- There are certain matters specified in the Companies Act 2013, which may be discussed at meeting only if a special notice is given at least 14 days before the meeting.

- The following matters require special notice.

- To remove the director before the expiry of his period.

- To appoint a director in the place of a director so removed.

- To re-appoint the retiring Auditor.

Answer :

Answer :