Tamilnadu State Board New Syllabus Samacheer Kalvi 12th Accountancy Guide Pdf Chapter 2 Accounts of Not-For-Profit Organisation Text Book Back Questions and Answers, Notes.

Tamilnadu Samacheer Kalvi 12th Accountancy Solutions Chapter 2 Accounts of Not-For-Profit Organisation

12th Accountancy Guide Accounts of Not-For-Profit Organisation Text Book Back Questions and Answers

I Multiple Choice Questions

Choose the correct answer

Question 1.

Receipts and payments account is a

(a) Nominal A/c

(b) Real A/c

(c) Personal A/c

(d) Representative personal account

Answer:

(b) Real A/c

![]()

Question 2.

Receipts and payments account records receipts and payments of

(a) Revenue nature only

(b) Captital nature only

(c) Both revenue and captial nature

(d) None of the above

Answer:

(c) Both revenue and captial nature

Question 3.

Balance of receipts and payments account indicates the

(a) Loss incurrd during the period

(b) Excess of income over expenditure of the period

(c) Total cash payments during the period

(d) Cash and bank balance as on the date

Answer:

(d) Cash and bank balance as on the date

Question 4.

Income and expenditure account is a

(a) Nominal A/c

(b) Real A/c

(c) Personal A/c

(d) Representative personal account

Answer:

(a) Nominal A/c

![]()

Question 5.

Income and expenditure Account is prepared to find out

(a) Profit or loss

(b) Cash and bank balance

(c) Surplus or deficit

(d) Financial position

Answer:

(c) Surplus or deficit

Question 6.

Which of the following should not be recorded in the income and expenditure account?

(a) Sale of old news papers

(b) Loss on sale of asset

(c) Honorarium paid to the secretary

(d) Sale proceeds of furniture

Answer:

(d) Sale proceeds of furniture

Question 7.

Subsceiption due but not received for the current year is

(a) An asset

(c) An expense

(b) A liability

(d) An item to be ignored

Answer:

(a) An asset

Question 8.

Legacy is a

(a) Revenue expenditure

(b) Capital expenditure

(c) Revenue receipt

(d) Capital receipt

Answer:

(d) Capital receipt

![]()

Question 9.

Donations received for a specific purpose is

(a) Revenue receipt

(b) Capital receipt

(c) Revenue expenditure

(d) Capital expenditure

Answer:

(b) Capital receipt

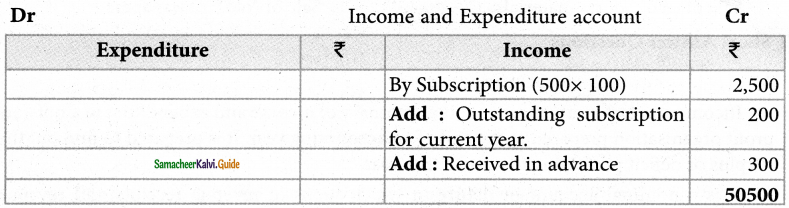

Question 10.

There are 500 members in a club each paying ₹ 100 as annual subscription. Subscription due but not received for the current year is ₹ 200; Subscription received in advance is ₹ 300. Find out the amount of subscription to be shown in the income and expend ; account.

(a) ₹ 50,500

(b) ₹ 50,200

(c) ₹ 49,900

(d) ₹ 49,800

Hint:

Answer:

(a) ₹ 50,500

II Very Short Answer Questions

Question 1.

State the meanting of not-for-profit organisation.

Answer:

Some organisations are established for the purpose of rendering servies to the public without any profit motive. They may be created for the promotion of art, culture, education, sports, etc. These organisations are called not-for-profit organisation.

![]()

Question 2.

What is receipts any payments account?

Answer:

Receipts and Payments account is a summary of cash and bank transactions of not-for- profit organisations prepared at the end of eac financial year.

It is a real account in nature. The receipts any payments account begins with the opening balances of cash and bank and ends with closing balances of cash and bank. All cash receipts are shown on the debit side and all cash payments are shown on the credit side of this account. All cash receipts and cash payments whether of capital or revenue nature will be recorded irrespective of the period for which the amoutn is received or paid, it is recorded if cash is received or paind during the year.

Question 3.

What is Legacy?

Answer:

A gift made to a not-for-profit organisation by a will, is called legacy. It is a capital receipt.

Question 4.

Write a short note on life membership fees.

Answer:

Amount received towards life membership fee from members is a capital receipt as it is non-recurring in nature.

Question 5.

Give four examples for Capital r pts of not-for-profit organisation.

Answer:

Life membership fees, Legacies Specifi, Specific donations, Sale of fixed assets, Special funds, Tournament fund prize

![]()

Question 6.

Give four examples for revenue receipts of not-for-profit organisation?

Answer:

Subscription, Interest on investment, Interest on fixed deposit

Sale of (old) sports materials, Sale of (old) newspapers

III Short Answer Questions

Question 1.

What is income and expenditure account?

Answer:

Income and expenditure account is a summary of income and expenditure of a not-for- profit organisation prepared at the end of an accounting year. It is prepared to find out the surplus or deficit pertaining to a particular year.

It is a nominal account in nature in which items of revenue receipts and revenue expenditure, relating to the current year alone are recorded. It is prepared following the accrual basis of accounting.

![]()

Question 2.

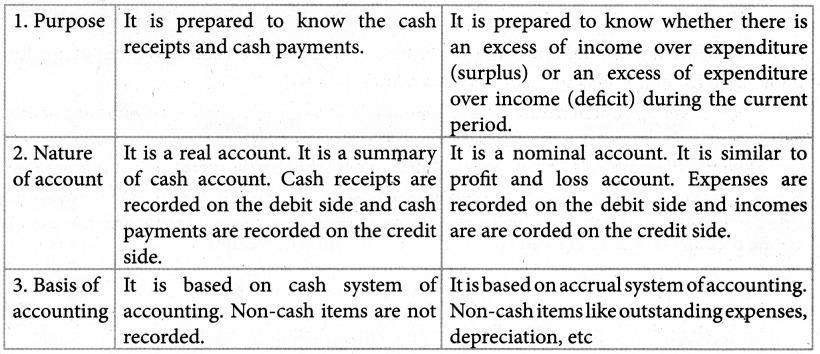

State the differences between Receipts and Payments Account and Income and Expenditure Account.

Answer:

Question 3.

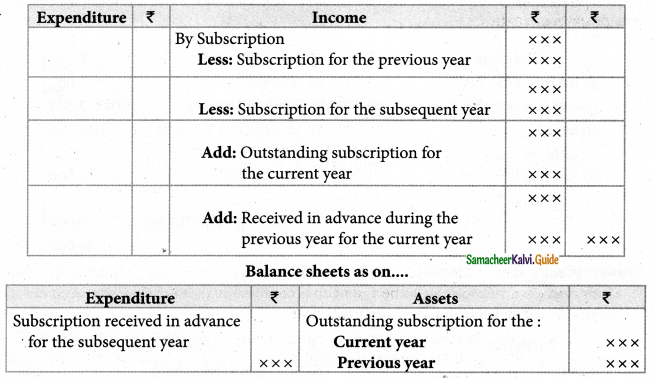

How annual subscription is dealt with in the final accounts of not-for-profit organisation?

Answer:

![]()

Question 4.

How the following items are dealt with in the final accounts of not-for-profit organisation? (a) Sale of sports materials (b) Life membership fees (c) Tournament fund

Answer:

- Sale of sports materials: Shown on the credit side of Income & Edpenditure A/c.

- Life membership fees: being capital receipt, will be shown on the liability side of the B/s.

- Tournament Fund: being capital receipt, will be shown on the liability side o f the B/s.

IV Exercise

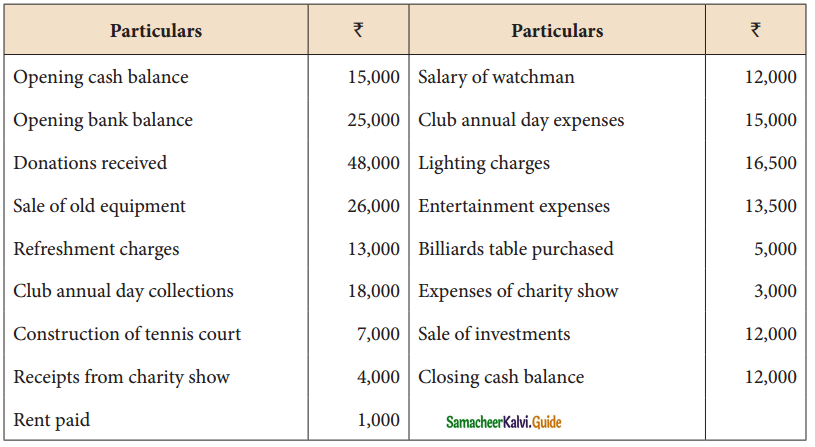

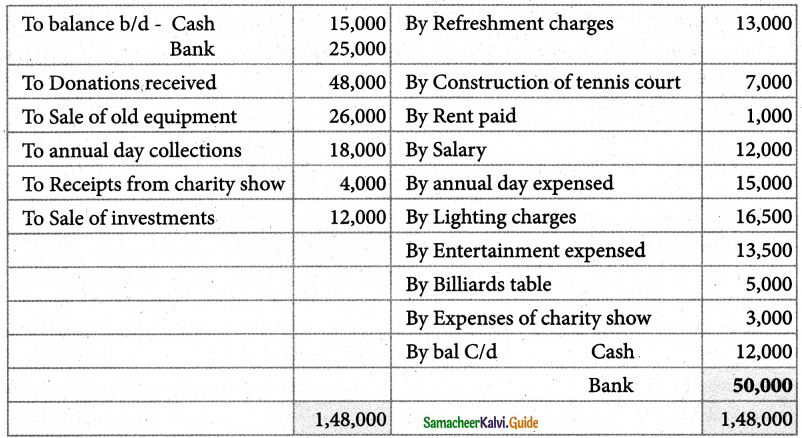

Question 1.

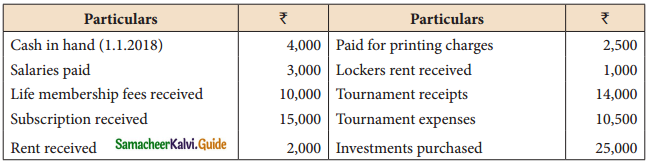

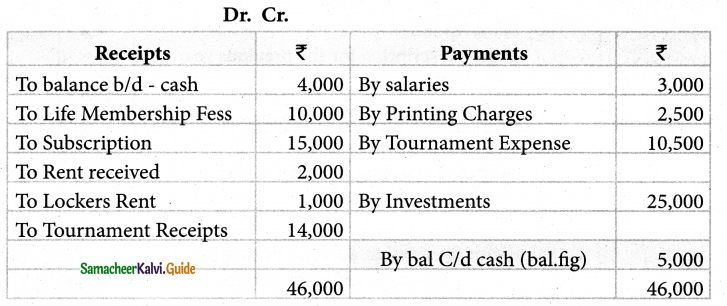

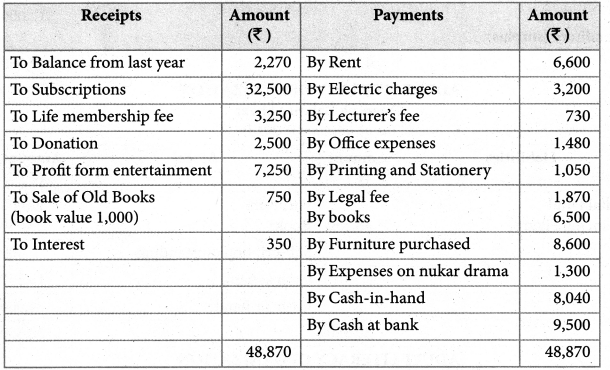

From the information given below, prepare Receipts and Payments account of Kurunji Sports Club for the year ended 31st December, 2018

Solution :

In the books of Kurunji Sports Club Receipts & Payments A/c for the year ended 31.12.2018

Answer:

Cash balance: ₹ 5,000

Question 2.

From the information given below, prepare Receipts and Payments account of Coimbatore Cricket club for the year ending 31st March, 2019.

Solution:

In the book of Coimbatore Cricket Club/Receipts & Payments A/c for the year ended 31.3.2019

Answer:

Bank balance: ₹ 2,400

(Hint: Wages yet to be paid is a non cash item. Hence, it is excluded in receipts and payments account)

![]()

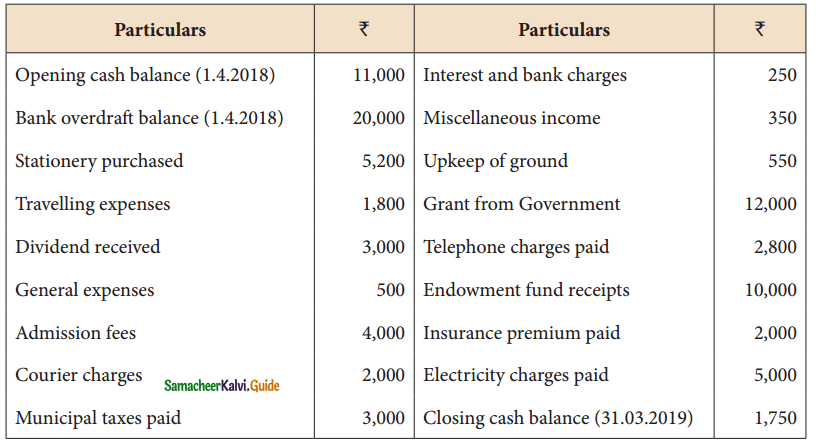

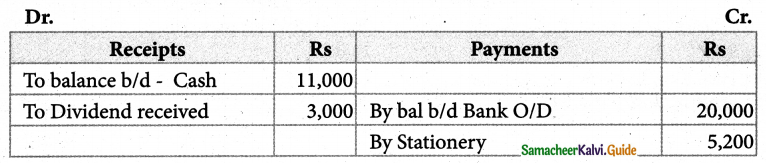

Question 3.

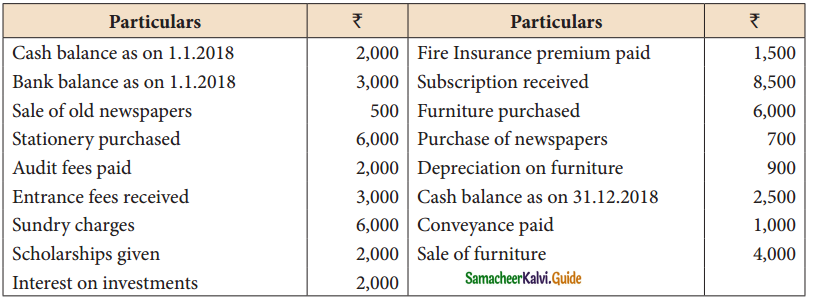

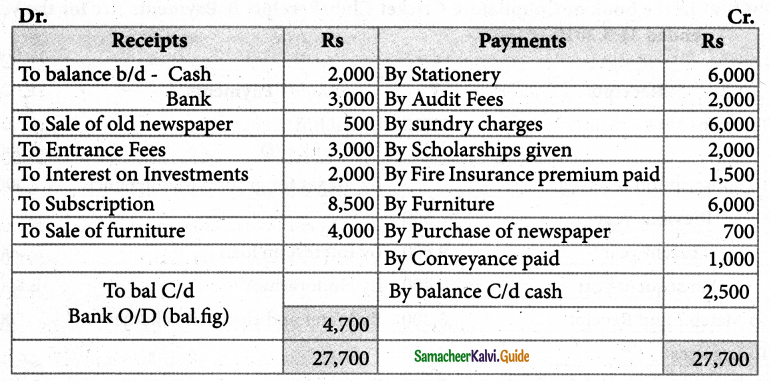

From the information given below, prepare Receipts and Payments account of Madurai Mother Theresa Mahalir Madram for the year ended 31st December, 2018.

Solution: In the book of Mother Teresa Mahalir Mandram, Madurai Receipt & Payment A/c for the year ended 31.12.2018

Answer:

Bank Overdraft: ₹ 4,700

(Hint: As depreciation on furniture is a non cash item, it is excluded in receipts and payments account)

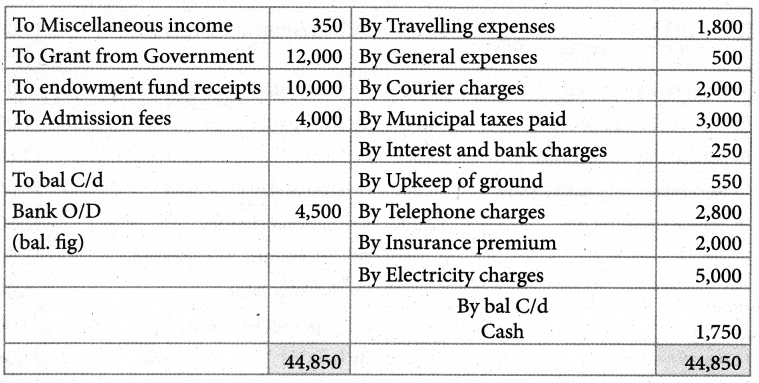

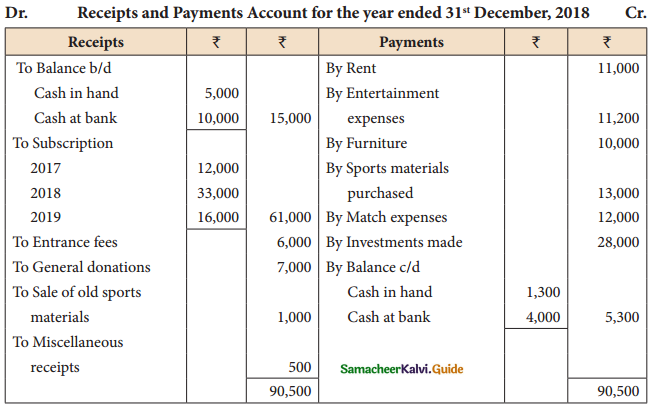

Question 4.

Mayiladuthrai Recreation Club gives you the following details. Prepare Receipts and Payments account for the year ended 31st March, 2019.

Solution:

In the books of Mayiladuthurai Recreation Club Receipts & Payments A/c for the year ended 31.3.2019

Answer:

Bank balance: ₹ 50,000

![]()

Question 5.

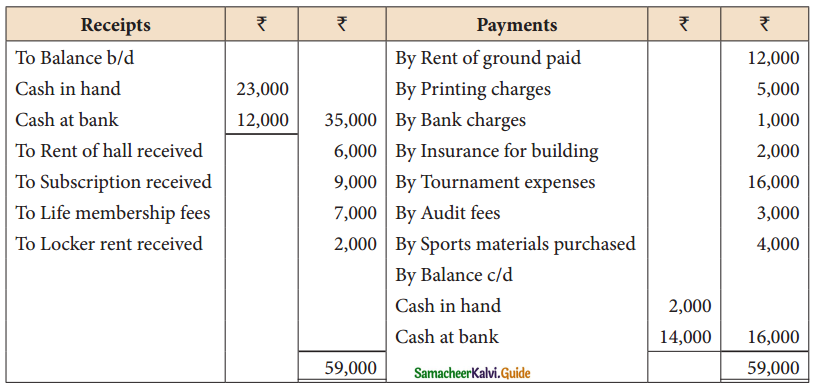

From the following information, prepare Receipts and Payments account of Cuddalore Kabaddi Association for the year ended 31st March, 2019

Solution :

In the books of Cuddalore Kabaddi Association

Receipts & Payments A/c for the year ended 31.3.2019

Answer:

Bank Overdraft: ₹ 4,500

Question 6.

From the following receipts and payments account of Tenkasi Ihiruvalluvar Mandram, Prepare income and expenditure account for the year ended 31st March, 2019.

In the books of Tenkasi Ihiruvalluvar Mandram Income &Expenditure A/c for the year ended 31.3.19

Answer:

Surplus: ₹14,000

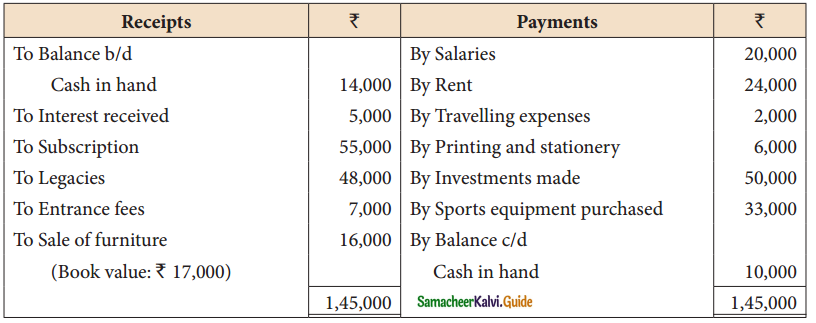

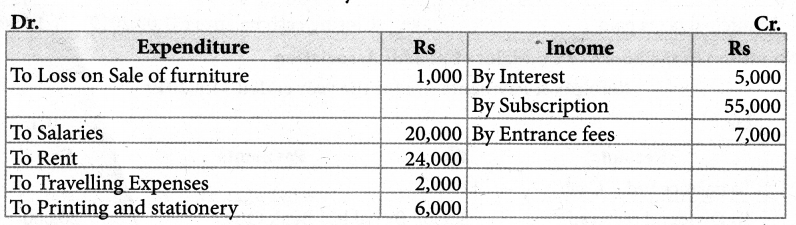

Question 7.

From the following receipts and payment account, prepare income and expenditure account of Kumbakonam Basket Ball Association for the year ended 31st March, 2018.

Solution: In the books of Kumbakonam Basket Ball Association Income &Expenditure A/cfor the year ended 31.3.18

Answer:

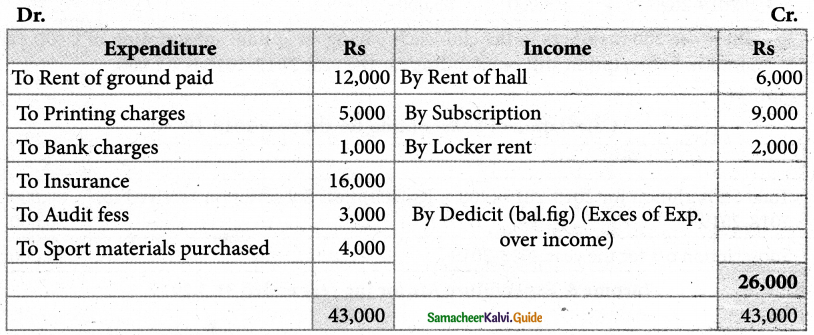

Deficit: ₹ 26,000

![]()

Question 8.

From the following receipts and payments account and the additional information given below, calculate the amoumt of of subscription to be shown in Income and expenditure account for the year ending 31st December, 2018.

Additional information: Subscription outstanding for the year 2018 is Rs.8,000

Solution:

Income & Expenditure A/c for the year ended 31.12.2018

Answer:

Subscription for 2018: ₹ 1,80,000)

Question 9.

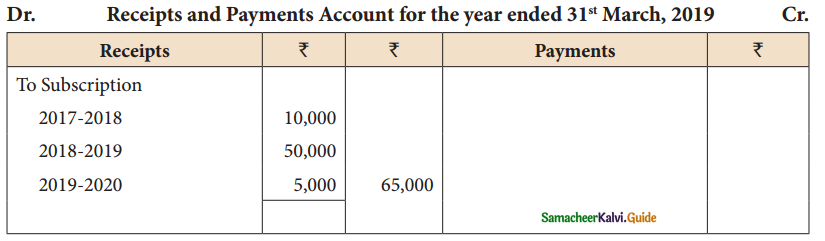

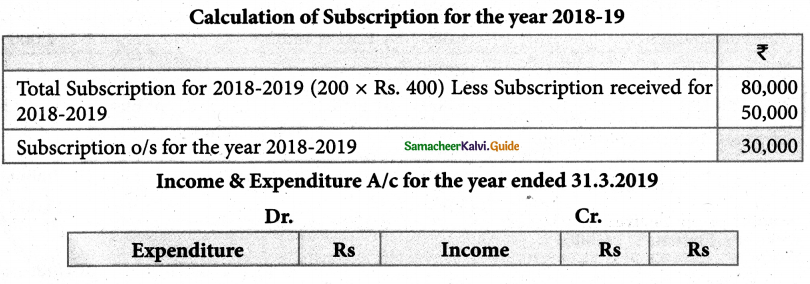

How the following items will appear in the final accounts of a club for the year ending 31st March 2019?

There are 200 members in the club each paying an annual subscription of ₹ 400 per annum. Subscription still outstanding for the year 2017-2018 is ₹ 2,000.

Solution :

Answer:

Income and Expenditure A/c: Subscription: ₹ 80,000 Balance Sheet: Assets: Subscription outstanding: ₹ 32,000; Liabilities: Subscription received in advance: ₹ 5,000

![]()

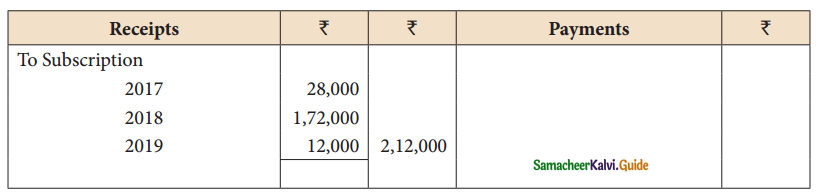

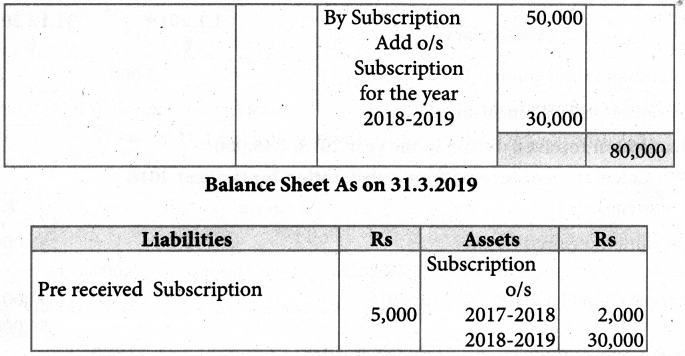

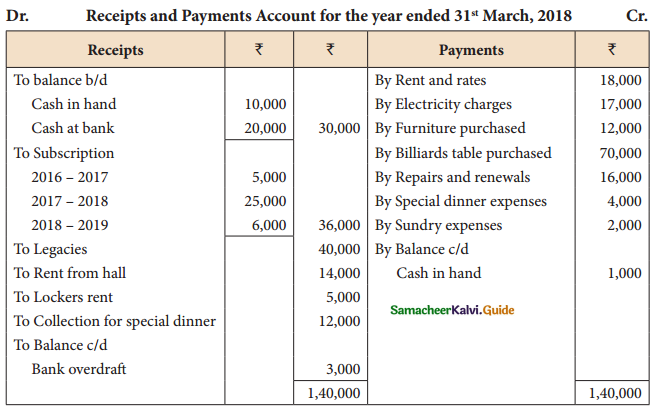

Question 10.

Ho w will the following items appear in the final accounts of a club for the year ending 31st March 2017? Received subscription of ₹ 40,000 during the year 2016-17. This includes subscription of ₹ 5,000 for 2015-16 and ₹ 3,000 for the year 2017-18. subscription of ₹ 1,000 is still outstanding for the year 2016-17.

Solution:

Income & Expenditure A/c for the year ended 31.3.17

Answer:

Income and Expenditure A/c: Subscription: ₹ 33,000

Balance Sheet: Assets: Subscription outstanding: ₹ 1,000;

Liabilities: Subscription received in advance: ₹ 3,000

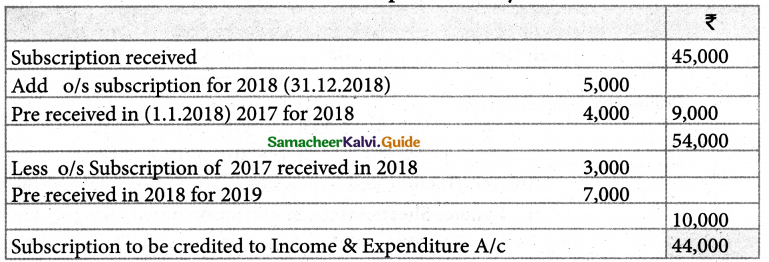

Question 11.

Compute income from subscription for the year 2018 from the following particulars relating to a club.

Subscription received during in the year 2018: ₹ 45,000

Solution:

Calculation of income from subscription for the year 2018

Answer:

Income and Expenditure A/c: Subscription: ₹ 44,000

![]()

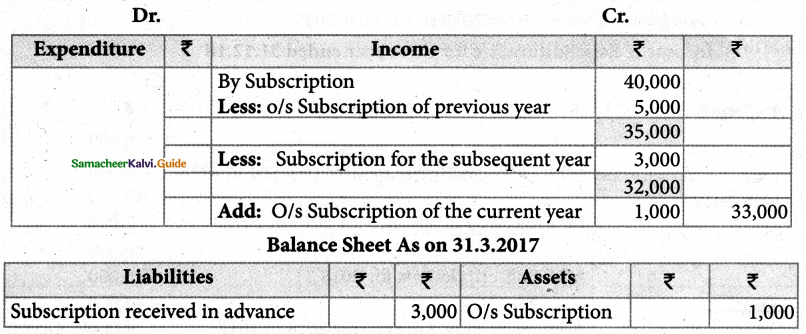

Question 12.

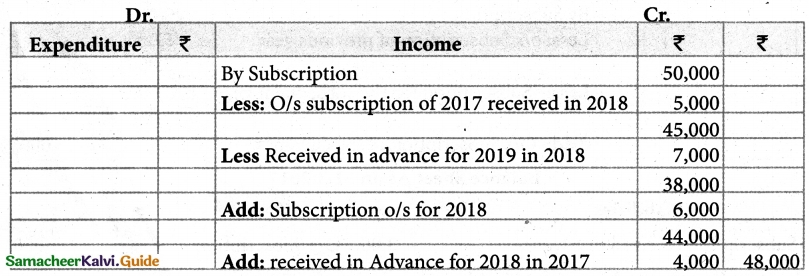

From the following particulars, show how the item ‘Subscription’ will appear in the Income and Expenditure Account for the year ended 31.12.2018?

Subscription received in 2018 is ₹ 50,000 which includes ₹ 5,000 for 2017 and ₹ 7,000 for 2019. Subscription outstanding for the year 2018 is ₹ 6,000. Subscription of ₹ 4,000 was received in advance for 2018 in the year 2017.

Solution:

Income & Expenditure A/c for three year ended 31.12.18

Answer:

Income and Expenditure A/c: Subscription:₹ 48,000

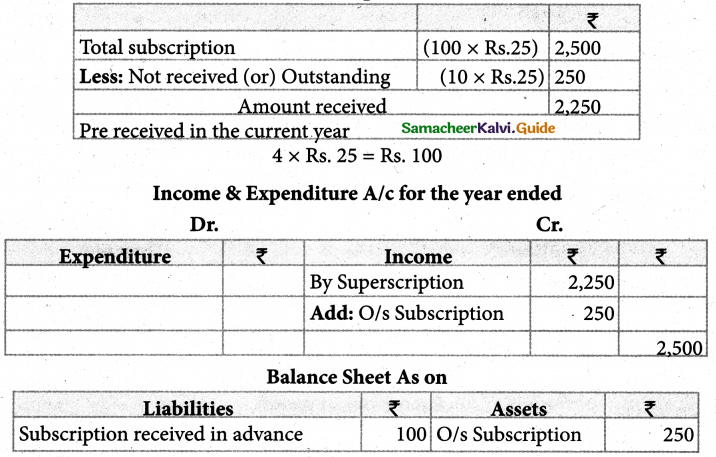

Question 13.

How the following items appear in the final accounts of Thoothukudi Young Pioneers Association?

There are one hundred members in the association each paying 25 as annual subscription. By the end of the year 10 members had not paid their subscription but four members had paid for the next year in advance.

Solution:

Calculation of income from subscription

Answer:

Income and Expenditure Account: Subscription: ₹ 2,500

Balance Sheet: Assets: Subscription outstanding: ₹ 250;

Liabilities: Subscription received in advance: ₹ 100

![]()

Question 14.

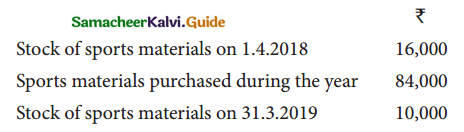

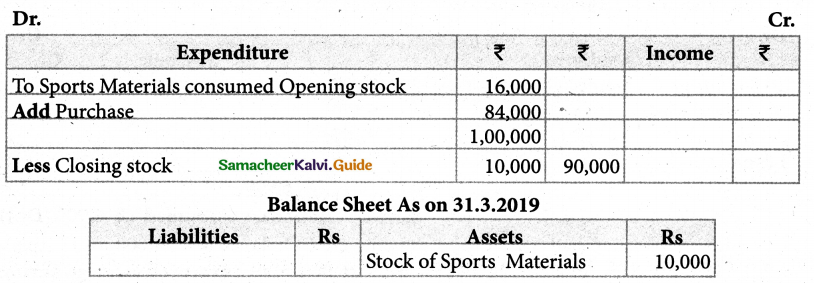

How will the following appear in the final accounts of Marthadam Women Cultural Association?

Solution :

Income & Expenditure A/c for the year ended 31.3.2019

Answer:

Income and Expenditure Account (Dr): ₹ 90,000;

Balance Sheet: Assets: Stock of sports materials: ₹ 10,000

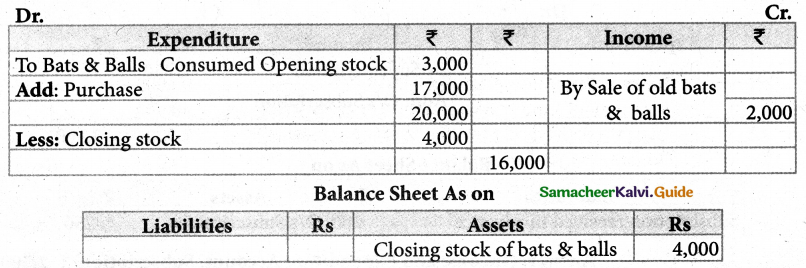

Question 15.

How will the following appear in the final accounts of Vedaranyam Sports Club?

| ₹ | |

| Opening stock of bats and balls | 3,000 |

| Purchase of bats and balls during the year | 17,000 |

| Sale of old bats and balls | 2,000 |

| Closing stock of bats and balls | 4,000 |

Solution:

Income & Expenditure A/c for the year ended

Answer:

Income and Expenditure Account: Bats and balls consumed : ₹ 16,000 (Dr);

Sale of old sports materials: ₹ 2,000 (Cr.)

Balance Sheet: Assets side: Stock of bats and balls: ₹ 4,000)

![]()

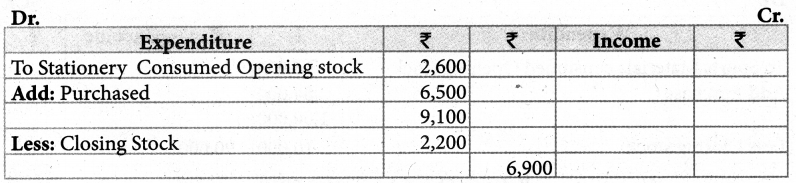

Question 16.

Show how the following items appear in the income and expenditure account of Sirkazhi Singers Association?

| ₹ | |

| Stock of stationery on 1.4.2018 | 2,600 |

| Purchase of stationery during the year | 6,500 |

| Stock of stationery on 31.3.2018 | 2,200 |

Solution:

Income & Expenditure A/c for the year ended 31.3.2018

Answer:

Stationery consumed : ₹ 6,900 (Dr.)

Question 17.

Chennai tennis club had Match fund showing credit balance of ₹ 24,000 on 1st April, 2018. Receipt to the fund during the year was ₹ 26,000. Match expensed incurred during the year was ₹ 33,000. How these items will appear in the final accounts of the club for the year ended 31st March, 2019?

Solution:

Balance Sheet As on 31.3.19

Answer:

Balance sheet: Liabilities: Match fund : ₹ 17,000

![]()

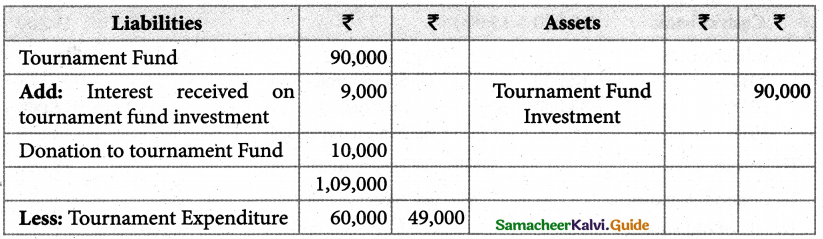

Question 18.

How will the following appear in the final accounts of Karaikudi sports club for the year ending 31st March, 2019?

Particulars ?

| Particular | ₹ |

| Tournament fund on 1st April 2018 | 90,000 |

| Tournament fund investment on 1st April 2018 | 90,000 |

| Interest received on tournament fund investment | 9,000 |

| Donation to tournament fund | 10,000 |

| Tournament expenses | 60,000 |

Solution:

Balance Sheet As on 31.3.2019

Answer:

Balance sheet: Liabilities: Tournament fund: ₹ 49,000

Assets: Tournament fund investment: ₹ 90,000

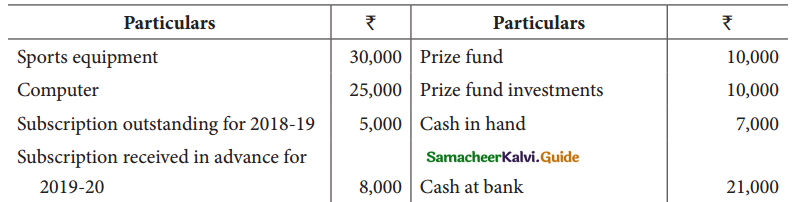

Question 19.

Compute capital fund of Salam Sports Club as on 01.4.2019?

Solution:

Balance Sheet As on 1.4.2019

Answer:

Capital fund: ₹ 80,000

![]()

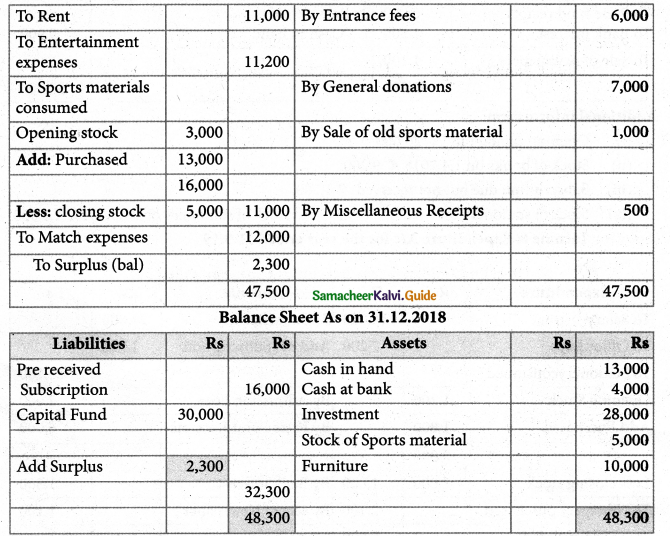

Question 20.

From the follwoing Receipts and Paymentaccount and from the information given below of Ramanathapuram Sports Club, prepare Income and Expenditure account for the year ended 31st December, 2018 and the balance sheet as on that date.

Additional information:

(i) Capital fund as on 1st January 2018 ₹ 30,000

(ii) Opening stock of sports material ₹ 3,000 and closing stock of sports material ₹ 5,000

Solution

Dr. Income & Expenditure A/c for three year ended 31.12.18

Answer:

Surplus: ₹ 2,300; Balance Sheet total: ₹ 48,300

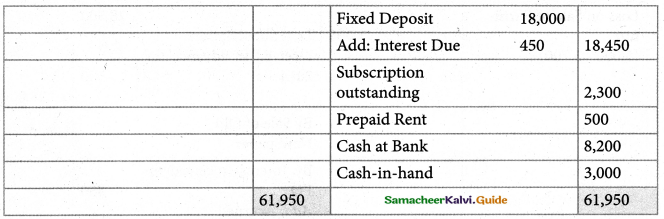

![]()

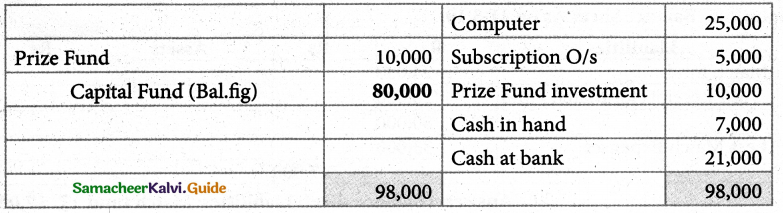

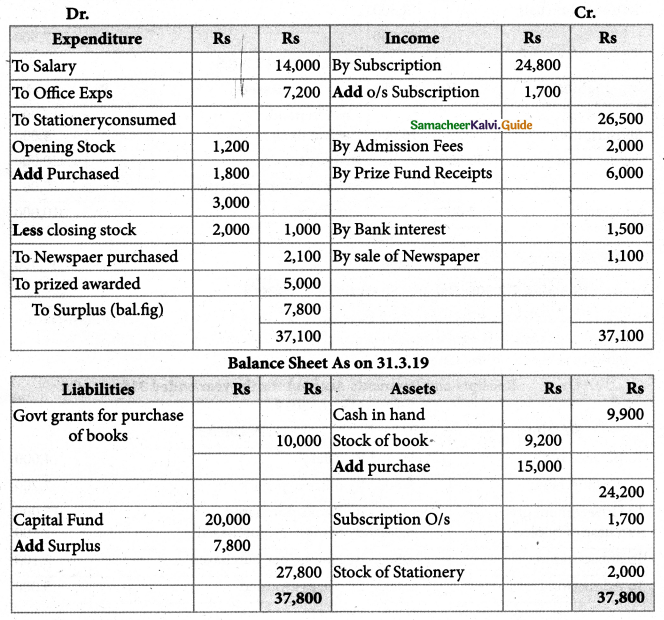

Question 21.

From the following Receipts and Payments account of Yarcaud Youth Association, prepare Income and expenditure account for the year ended 31st March, 2019 and the balance sheet as on the date.

Additional information:

(i) Opening capital fund ₹ 20,000.

(ii) Stock of books on 1.4.2018 ₹ 9,200.

(iii) Subscription due but not received ₹ 1,700.

(iv) Stock of stationery on 1.4.2018 ₹ 1,200 and stock of stationery on 31.3.2019, ₹ 2,000

Solution:

Income & Expenditure A/c for the year ended 31.3.19

Answer:

Surplus: ₹ 7,800; Balance Sheet total: ₹ 37,800

![]()

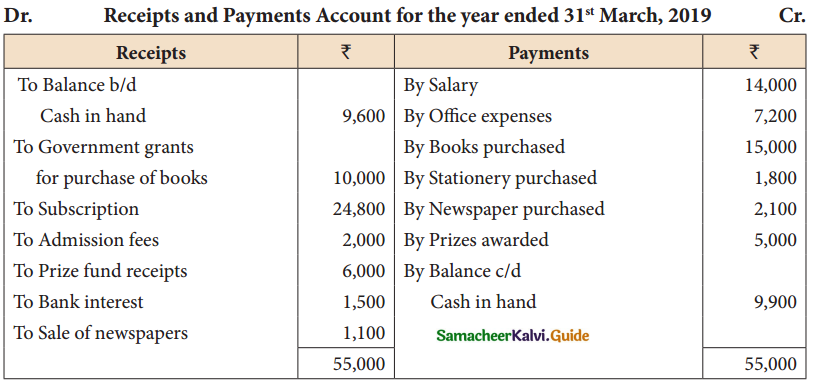

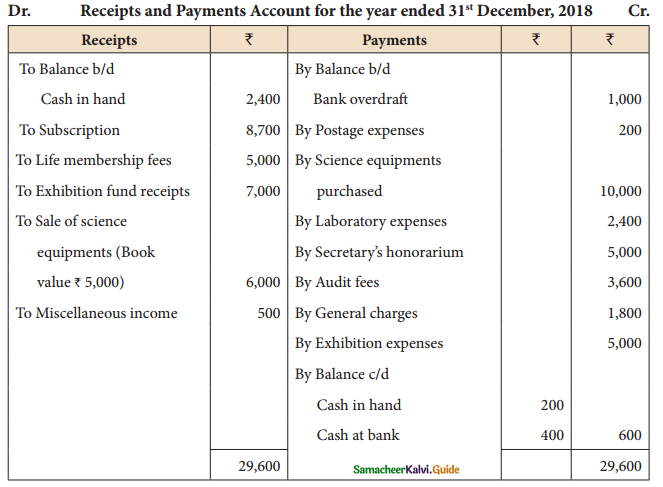

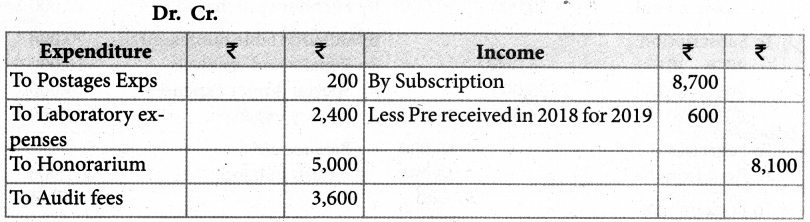

Question 22.

Following is the Receipts and Payments account of Neyveli Science Club for the year ended 31st December, 2018.

i

Additional information:

(i) Opening capital fund ₹ 6,400.

(ii) Subscription includes ₹ 600 for the year 2019.

(iii) Science equipment as on 1.1.2018 ₹ 5,000.

(iv) Surplus on account of exhibition should be kept in reserve for new auditorium. Prepare income and expenditure account for the year ended 31st December, 2018 and the balance sheet as on that date.

Solution:

Income & Expenditure A/c for the year ended 31.12.18

Answer:

Deficit: ₹ 1,400; Balance Sheet total: ₹ 10,600

![]()

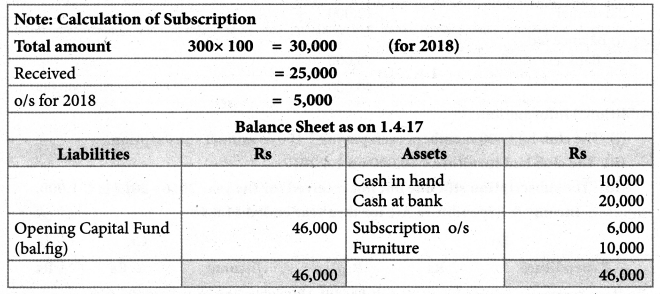

Question 23.

From the following Receipts and Payments account of Sivasasi Pensioner’s Recreation Club, prepare income and expenditure account for the year ended 31st March, 2018 and the balance sheet as on that date.

Additional information:

(i) The club had 300 members each paying ₹ 100 as annual subscription.

(ii) The club had furniture ₹ 10,000 on 1.4.2017.

(iii) The subscription still due but not received for the year 2016 – 2017 is ₹ 1,000.

Solution:

Income & Expenditure A/c for thre year ended 31.3.18

Answer:

Surplus: ₹ 4,000; Opening capital fund ₹ 46,000; Balance sheet total: ₹ 99,000

![]()

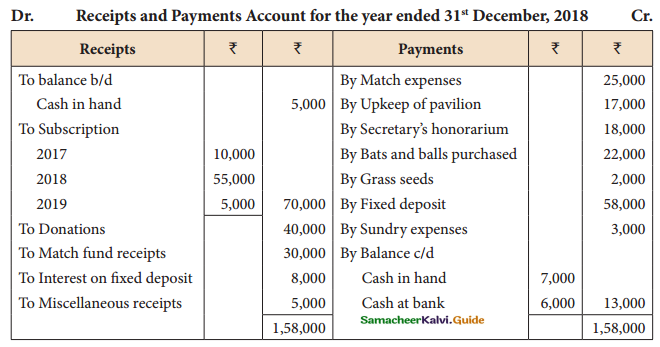

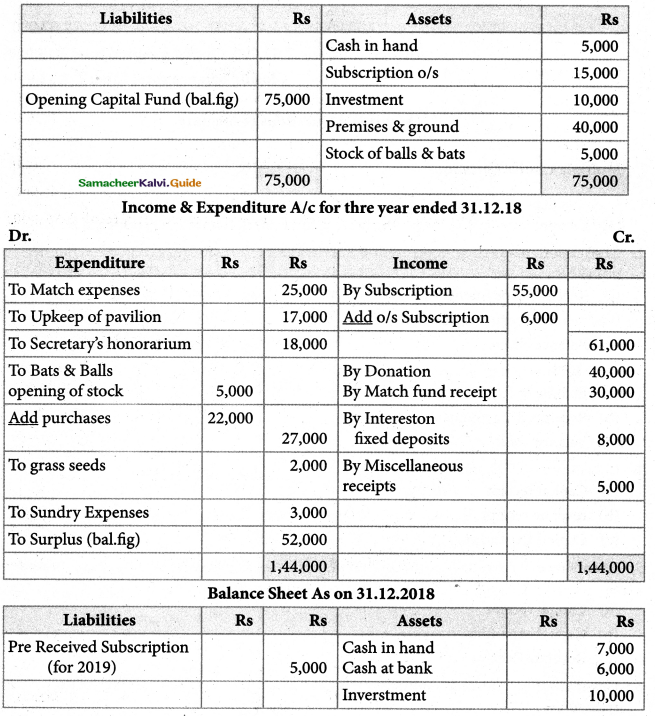

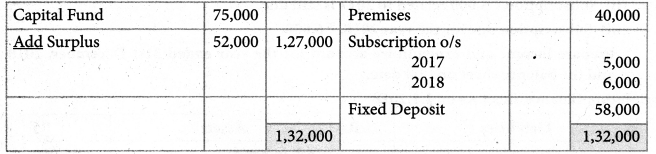

Question 24.

Following is the Receipts and payments account ofVirudhunagar Volleyball Association for the year ended 31st December, 2018.

Additional information:

(i) On 1.1.2018, the association owned investments ₹ 10,000, premises and grounds ₹ 40,000, stock of bats and balls ₹ 5,000.

(ii) Subscription 15,000 related to 2017 is still due.

(iii) Subscription due for the year 2018, ₹ 6,000.

Prepare income and expenditure account for the year ended 31st December, 2018 and the balance sheet on that date.

Solution :

Balance Sheet As on 1.1.2018

Answer:

SurpIus: ₹ 52,000; Opening capital fund ₹ 75,000;

Closing balance sheet total: ₹ 1,32,000

12th Accountancy Guide Accounts of Not-For-Profit Organisation Additional Important Questions and Answers

I Multiple Choice Questions

Question 1.

Receipts & payments A/c records receipts & payments of

(a) Current year only

(b) Previous & future period only

(c) both a & b

Answer:

(c) both a & b

![]()

Question 2.

Non-cash items such as depreciation outstanding expenses and accrued income are not shown in

(a) Receipts & payments A/c

(b) Income & expenditure A/c

(c) Balance sheet

Answer:

(a) Receipts & payments A/c

Question 3.

Only revenue items are recorded in

(a) Income & Expenditure A/c

(b) Receipts & payments A/c

(c) Balance sheet

Answer:

(a) Income & Expenditure A/c

Question 4.

Interest on investment received is a

(a) Capital receipt

(b) revenue receipt

(c) Capital Expenditure

Answer:

(b) revenue receipt

![]()

Question 5.

Grants received towards construction of buildings acqisiton of assets etc are treated as

(a) Capital receipt

(b) Capital expenditure

(c) Revenue Receipt

Answer:

(a) Capital receipt

Question 6.

Grants received towards maintenance of assets, payments of salaries etc aire are treated as

(a) Capital receipt

(b) revenue receipt

(c) Capital Expenditure

Answer:

(b) revenue receipt

Question 7.

Revenue items of current year alone are recorded in

(a) Receipts & Payments A/c

(b) Income & Expenditure A/c

(c) Balance sheet

Answer:

(b) Income & Expenditure A/c

III. Short Answer Questions

Question 1.

What are the ffeatures of not-for-profit organisations.

Answer:

Following are the features of not-for-profit organisations:

- Not-for-profit organisations are the organisations which function without any profit motive.

- Their main aim is to provide services to a specific group or the public at large.

- Generally, they do not undertake business or trading activities.

- Their main sources of income include subscription from members, donations, grant-in¬aid and legacies.

![]()

Question 2.

What are the accounts prepared by not-for-profit organisations

Answer:

- Receipts and payments account,

- Income and expenditure account and

- Balance sheet

Question 3.

What are the steps in the preparation of Receipts & Payments A/c?

Answer:

Following are the steps involved in the preparation of receipts and payments account:

- Record the opening balance of cash in hand and favourable bank balance on the debit side of receipts and payments account. If there is bank overdraft, it must be recorded on the credit side.

- Actual cash receipts during the year are recorded on the debit side and actual cash payments during the year are recorded on the credit side.

- While recording cash receipts and payments, no distinction needs to be made between revenue and capital items. Similarly, no distinction needs to be made whether the amount reveived or paid relates to the current period, previous period or future period.

- If the total of the debit side is more than the credit side, the balancing figure will appear on the credit side. It represents the closing balance of cash or bank.

- If the total of the credit side is more than the debit side, the balancing figure will appear on the debit side. It represents bank overdraft.

Question 4.

Name a few examples capital for expenditure & revenue expenditure.

Answer:

| Capital expenditure | Revenue expenditure |

| Purchase of sports equipment Purchase of books for library | Honorarium Charity Audit fees Purchase of sports materials Printing and stationery Postage and courier charges Expenses relating to a) Tournament, b) Sports, c) Matches, d) Enterainments e) Dinner |

IV Additional Problems:

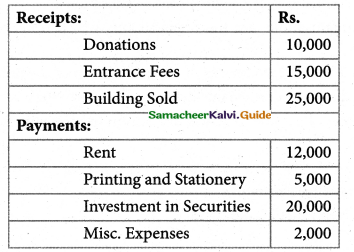

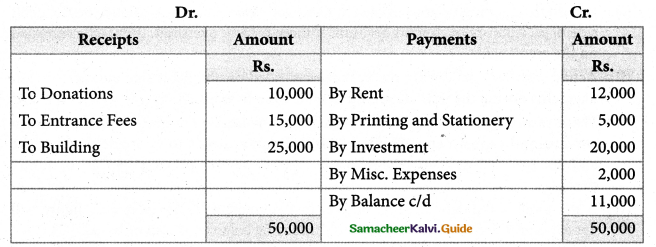

Question 1.

The following particulars of a club are available.

Prepare Receipts and Payments Account as on 31st March, 2002.

Solution:

Receipts and Payments A/c for the year ended 31st March, 2002

![]()

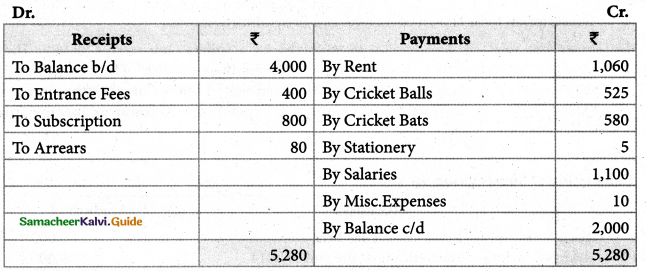

Question 2.

From the following particulars prepare receipts and payments account of a club for the year 2000:

Cash Balance (1st Jan. 2001) Rs. 4,000; Entry fee received Rs. 400; Subscription received Rs. 800; Last year’s arrears Rs. 80; Rent paid Rs. 1,060; Purchase of cricket balls Rs. 525; Purchase of cricket bats Rs. 580; Miscellaneous expenses Rs. 10; Purchase of Stationery Rs. 5; Salary paid Rs. 1,100.

Solution:

Receipts and Payments A/c for the year ended 31st December, 2001

Question 3.

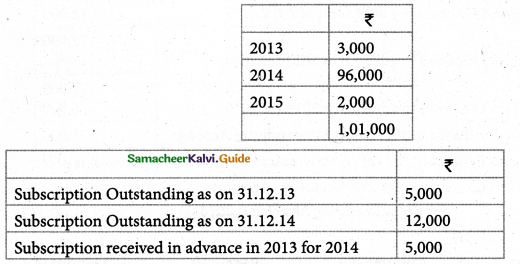

Subscription received by the Health Club during the year 2014 were as under:

Calculate the amount of Subscription to be shown on the income side of Income and Expenditure A/c.

Solution:

Calculation of Subscription for 2014

| Receipts | Amounts |

| Total Subscription Received during 2014 Add: Subscription Outstanding at 31.12.14 | 1,01,000 12,000 |

| Less: Subscription Outstanding 31.12.13 | 1,13,000 5,000 |

| Add: Subscription received in advance in 2013 for 2014 | 1,08,000 5,000 |

| Less: Subscription received in advance in 2014 for 2015 | 1,13,000 2,000 |

| Subscription to be shown in Income and Expenditure Account | 1,11,000 |

![]()

Question 4.

During the year 2014, subscription received by a sports club were ₹ 80,000. These included ^ 3,000 for the year 2013 and 16,000 for the year 2015. On Decembrer 31, 2013 amount of subscription due but not reveived was ₹ 12,000. Calculate the ammount of subscription to be shown in Income and Expenditure Account as income from subscription?

Solution

Calculation of Subscription for 2014

| Receipts | Amount |

| Total Subscription Received during 2014 Add: Subscription Outstanding at the end of 2014 | 80,000 9,000 |

| Less: Subscription Outstanding at the end of 2013 | 89.000 12.000 |

| Add: Subscription received in advance in 2013 for 2014 | 77,000 …………. |

| Less: Subscription received in advance in 2014 for 2015 | 77,000 6,000 |

| Subscription to be shown in Income and Expenditure Account | 71,000 |

Question 5.

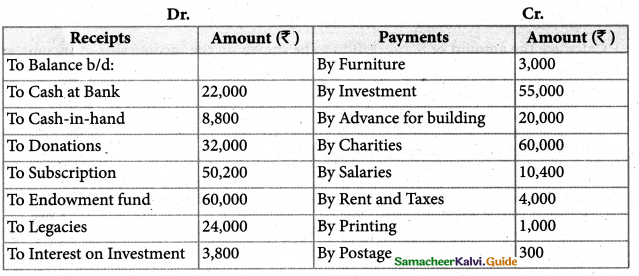

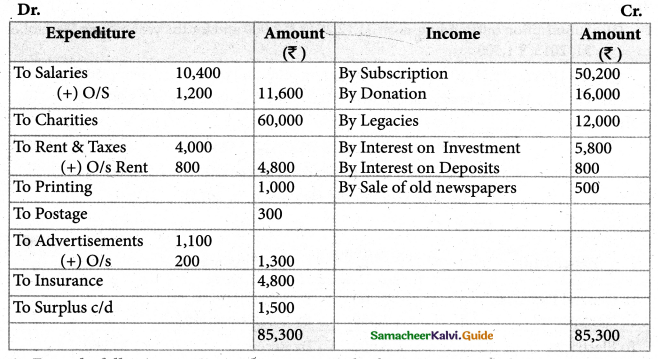

The Receipts and Payments Account of Harimohan Charitable Institution is given:

Prepare the Income and Expenditure Account for the year ended on March 31, 2014 after considering the following:

(i) It was decided to treat 50% of the amount received on account of Legacies and Donations as income.

(ii) Liabilities to be provided for are: Rent’ 800; Salaries ‘ 1200; Advertisement’ 200

(iii) ‘2,000 due for interest on investment was not actually received.

Solution:

Income & Expenditure A/c the year ended 31.03.2018

![]()

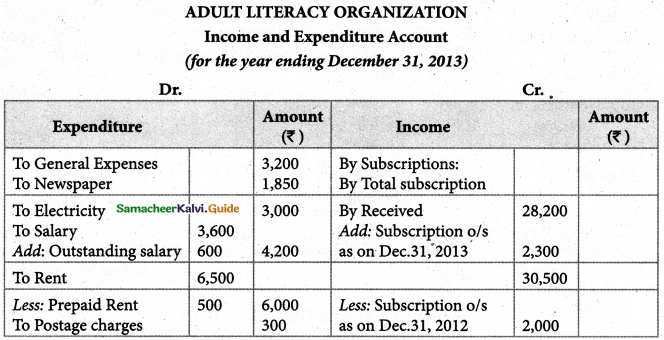

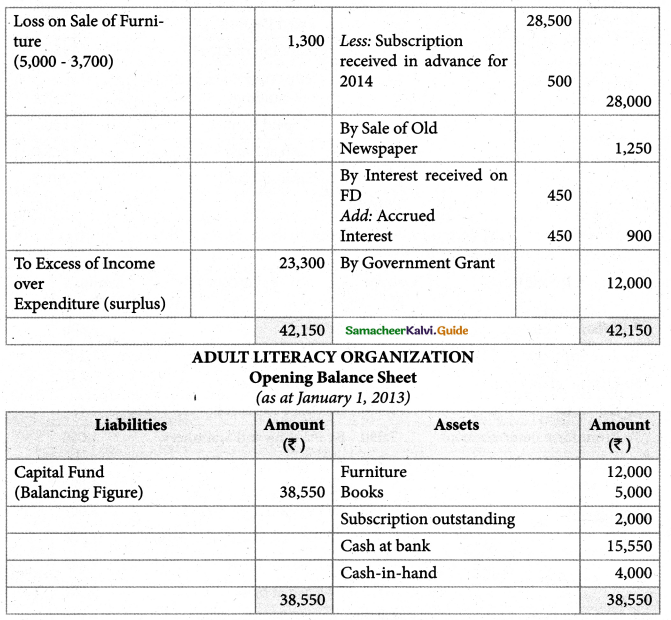

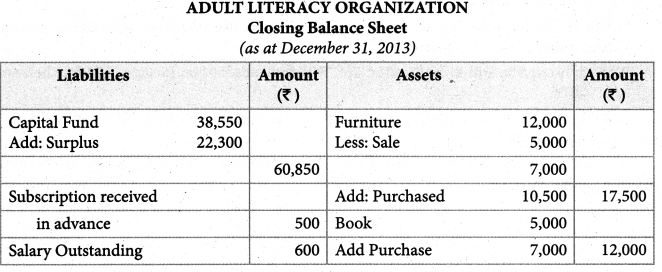

Question 6.

From the following receipts and payments and information given below, prepare Income and Expenditure Account and opening Balance Sheet of Adult Literacy orgnization as on December 31, 2013: Receipts and Payments Account for the year ending as on December31,2013.

Information:

(i) Subscription outstanding as on 31.12.2012, ₹ 2,000 and for the year ending December 31,2013, ₹ 1,500

(ii) On December 31,2013 Salary outstanding’ 600, and one month Rent paid in advance.

(iii) On Jan. 01,2012 organization owned Furniture ₹ 12,000, Books ₹ 5,000.

Solution:

![]()

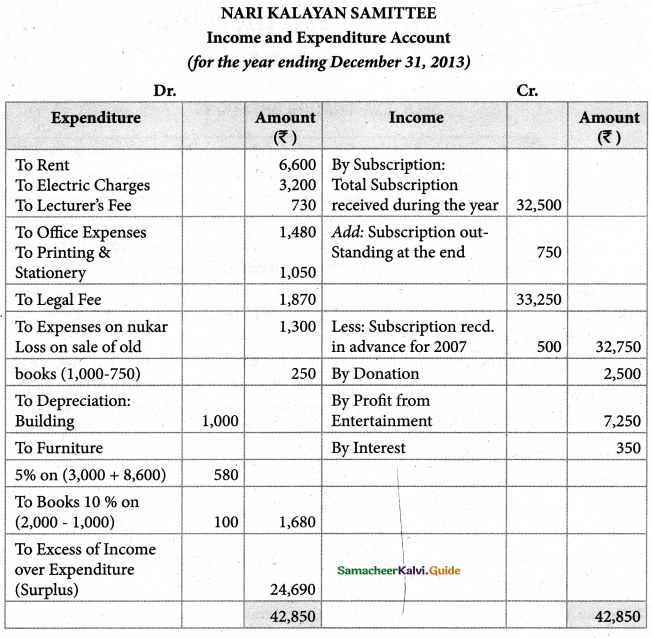

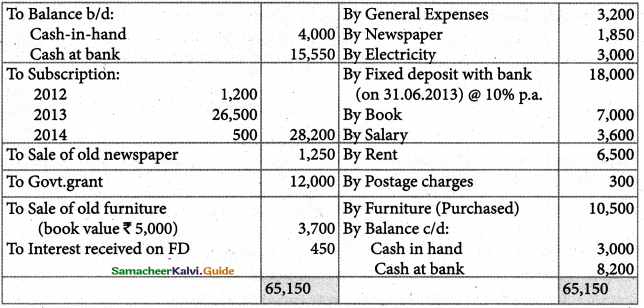

Question 7.

The following is the account of cash transactions of the Nari Kalayan Samittee for the year ended December 31, 2013:

You are required to prepare an Income and Expenditure Account after the following adjustments:

(i) Subscription still to be received are ‘ 750, but subscription include ‘ 500 for the year 2014.

(ii) In the beginning of the year the Sangh owned building ‘ 20,000 and furniture ‘ 3,000 and Books ‘2,000.

(iii) Provide depreciation of furniture @5% (including purchase), books @10% and building @5%.