Tamilnadu State Board New Syllabus Samacheer Kalvi 11th Accountancy Guide Pdf Chapter 6 Subsidiary Books – I Text Book Back Questions and Answers, Notes.

Tamilnadu Samacheer Kalvi 11th Accountancy Solutions Chapter 6 Subsidiary Books – I

11th Accountancy Guide Subsidiary Books – I Text Book Back Questions and Answers

![]()

I. Multiple Choice Questions

Choose the correct answer.

Question 1.

Purchases book is used to record ________.

a) all purchases of goods

b) all credit purchases of assets

c) all credit purchases of goods

d) all purchases of assets

Answer:

c) all credit purchases of goods

Question 2.

A periodic total of the purchases book is posted to the ________.

a) debit side of the purchases account

b) debit side of the sales account

c) credit side of the purchases account

d) credit side of the sales account

Answer:

a) debit side of the purchases account

Question 3.

Sales book is used to record ________.

a) all sales of goods

b) all credit sales of assets

c) all credit sales of goods

d) all sales of assets and goods

Answer:

c) all credit sales of goods

Question 4.

The total of the sales book is posted periodically to the credit of ________.

a) Sales account

b) Cash account

c) Purchases account

d) Journal proper

Answer:

a) Sales account

![]()

Question 5.

Purchase returns book is used to record ________.

a) returns of goods to the supplier for which cash is not received immediately

b) returns of assets to the supplier for which cash is not received immediately

c) returns of assets to the supplier for which cash is received immediately

d) None of the above

Answer:

a) returns of goods to the supplier for which cash is not received immediately

Question 6.

Sales return book is used to record ________.

a) Returns of goods by the customer for which cash is paid immediately

b) Returns of goods by the customer for which cash is not paid immediately

c) Returns of assets by the customer for which cash is not paid immediately

d) Returns of assets by the customer for which cash is paid immediately

Answer:

b) Returns of goods by the customer for which cash is not paid immediately

Question 7.

Purchases of fixed assets on credit basis is recorded in ________.

a) Purchases book

b) Sales book

c) Purchases returns book

d) Journal proper

Answer:

d) Journal proper

Question 8.

The source document or voucher used for recording entries in sales book is ________.

a) Debit note

b) Credit note

c) Invoice

d) Cash receipt

Answer:

c) Invoice

Question 9.

Which of the following statements is not true?

a) Cash discount is recorded in the books of accounts

b) Assets purchased on credit are recorded in journal proper

c) Trade discount is recorded in the books of accounts

d) 3 grace days are added while determining the due date of the bill

Answer:

c) Trade discount is recorded in the books of accounts

Question 10.

Closing entries are recorded in ________.

a) Cash Book

b) Journal Proper

c) Ledger

d) Purchases book

Answer:

c) Ledger

![]()

II. Very Short Answer Type Questions

Question 1.

Mention four types of subsidiary books.

Answer:

The following are the four types of subsidiary books.

- Cash book

- Purchases book

- Sales book

- Bills receivable book

Question 2.

What is purchases book?

Answer:

- Purchases book is a subsidiary book in which only credit purchases of goods are recorded.

- While recording transactions in the purchases book, it must be ascertained whether the credit purchase is related to the item in which the firm is dealing.

- Purchases of assets and purchase of goods for cash are not entered in purchases book.

Question 3.

What is purchases returns book?

Answer:

- Purchases returns book is a subsidiary book in which transactions relating to return of previously purchased goods to the suppliers, for which cash is not immediately received are recorded.

- Since goods are going out to the suppliers, they are also known as returns outward and the book is called as ‘returns outward book or returns outward journal’.

Question 4.

What is sales book?

Answer:

- Sales book is a subsidiary book maintained to record credit sale of goods. Goods mean the items in which the business is dealing.

- These are meant for regular sale.

- Cash sale of goods and sale of property and assets whether for cash or on credit are not recorded in the sales book.

- This book is also named as sales day book, sold day book, sales journal or sale register.

Question 5.

What is sales returns book?

Answer:

- Sales returns book is a subsidiary book, in which, details of return of goods are sold for which cash is not immediately paid are recorded.

- This book is not concerned with the return of assets or return of goods for which cash is paid. <$> This book is prepared just like the other day books.

![]()

Question 6.

What is debit note?

Answer:

- A ‘debit note’ is a document, bill or statement sent to the person to whom goods are returned.

This statement informs that the supplier’s account is debited to the extent of the value of goods returned. - It contains the description and details of goods returned, name of the party to whom goods are returned and net value of the goods so returned with reason for return.

Question 7.

What is credit note?

Answer:

- A credit note is prepared by the seller and sent to the buyer when goods are returned indicating that the buyer’s account is credited in respect of goods returned.

- Credit note is a statement prepared by a trader who receives back from his customer the goods sold.

It contains details such as the description of goods returned by the buyer, quantity returned and also their value.

Question 8.

What is journal proper?

Answer:

- Journal proper is a residuary book which contains record of transactions, which do not find a place in the subsidiary books such as cash book, purchases book, and sales book, purchases returns book, sales returns book, bills receivable book and bills payable book.

- Journal proper or general journal is a book in which the residual transactions which cannot be entered in any of the sub divisions of journal are entered.

Question 9.

Define bill of exchange.

Answer:

According to the Negotiable Instruments Act, 1881, “Bill of exchange is an instrument in writing containing an unconditional order, signed by the maker, directing a certain person to pay a certain sum of money only to, or to the order of a certain person or to the bearer of the instrument”.

Question 10.

What is an opening entry?

Answer:

- At the end of the accounting year, all nominal accounts are closed but the business has to be carried on with previous year’s assets and liabilities.

- These accounts are to be brought into the accounts of the current year.

- Journal entry made in the beginning of the current year with the balances of assets and liabilities of the previous year is opening journal entry.

- In this entry, asset accounts are debited, liabilities and capital accounts are credited.

![]()

Question 11.

What Is an invoice?

Answer:

- Invoice is a business document or bill or statement, prepared and sent by the seller to the buyer giving the details of goods sold, such as quantity, quality, price, total value, etc.

- The invoice is a source document of prime entry both for the buyer and the seller.

III. Short Answer Questions

Question 1.

Give the format of purchases book.

Answer:

Question 2.

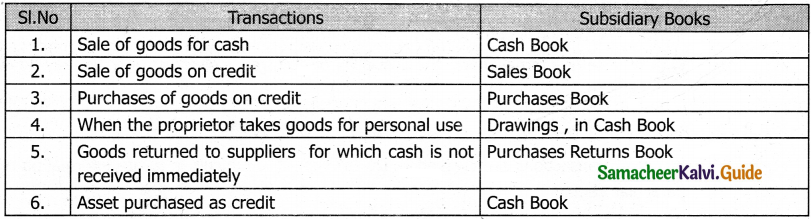

Mention the subsidiary books in which the following transactions are recorded.

Answer:

Question 3.

What are the advantages of subsidiary books?

Answer:

The advantages of maintaining subsidiary books can be summarised as under : Proper and systematic record of business transactions –

- All the business transactions are classified and grouped conveniently as cash and non cash ‘ transactions, which are further classified as credit purchases, credit sales, returns, etc.

- As separate books are used for each type of transactions, individual transactions are properly and systematically recorded in the subsidiary books.

Convenient posting:

- All the transactions of a particular nature are recorded at one place, i.e., in one of the subsidiary books.

- For example, all credit purchases of goods are recorded in the purchases book and ail credit sales of goods are recorded in the sales book.

- It facilitates posting to purchases account, sales account and concerned personal accounts.

Division of work:

As journal is sub-divided, the work will be sub-divided and different persons can work on different books at the same time and the work can be speedily completed.

Efficiency:

- The sub-division of work gives the advantage of specialisation. When the same work is done by a person repeatedly the person becomes efficient in handling it.

- Thus, specialisation leads to efficiency in accounting work.

Helpful in decision making:

- Subsidiary books provide complete details about every type of transactions separately.

- Hence, the management can use the information as the basis for deciding its future actions.

- For example, information regarding sales returns from the sales returns book will enable the management to analyse the causes for sales returns and to adopt effective measures to remove deficiencies.

Prevents errors and frauds:

- Internal check becomes more effective as the work can be divided in such a manner that the work of one person is automatically checked by another person.

- With the use of internal check, the possibility of occurrence of errors or fraud may be avoided or minimised.

Availability of requisite information at a glance:

- When all transactions are entered in one journal, it is difficult to locate information about a particular item.

- When subsidiary books are maintained, details about a particular type of transaction can be obtained from subsidiary books.

- The maintenance of subsidiary books helps in obtaining the necessary information at a glance.

Detailed Information available : As all transactions relating to a particular item are entered in a subsidiary book, it gives detailed information. It is easy to arrive at monthly or quarterly totals.

Saving in time : As there are many subsidiary books, work of entering can be done simultaneously by many persons. Thus, it saves time and accounting work can be completed quickly.

Labour of posting is reduced : Labour of posting is reduced as posting is made in periodical totals to the impersonal account, for example, Purchases account.

![]()

Question 4.

Write short notes on:

Answer:

a) Endorsement of a bill:

- Endorsement means signing on the face or back of a bill for the purpose of transferring the title of the bill to another person.

- The person who endorses is called the “Endorser”.

- The person to whom a bill is endorsed is called the “Endorsee”.

- The endorsee is entitled to collect the money.

b) Discounting of a bill:

- When the holder of a bill is in need of money before the due date of a bill, cash can be received by discounting the bill with the banker.

- This process is referred to as the discounting of bill.

- The banker deducts a small amount of the bill which is called discount and pays the balance in cash immediately to the holder of the bill.

IV. Exercises

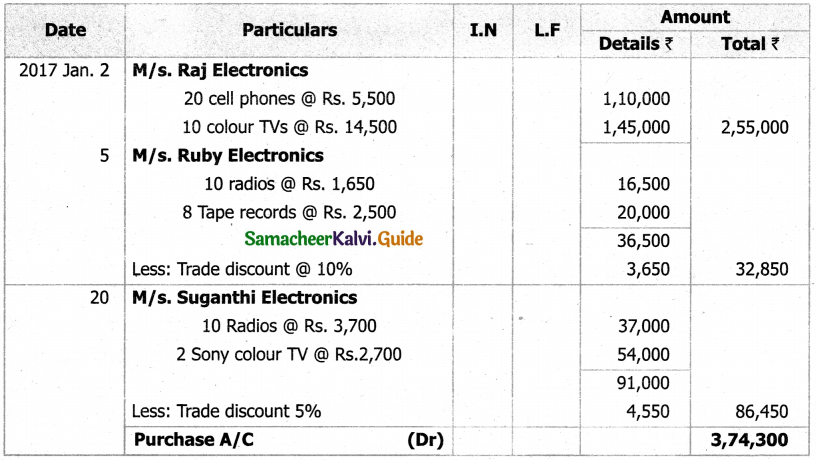

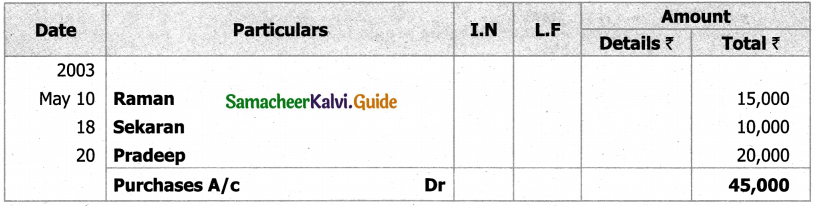

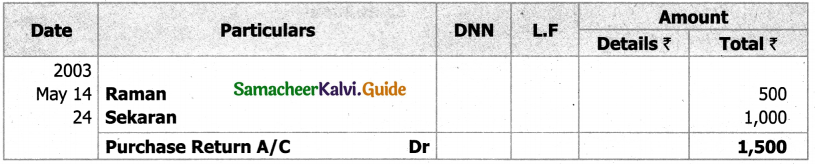

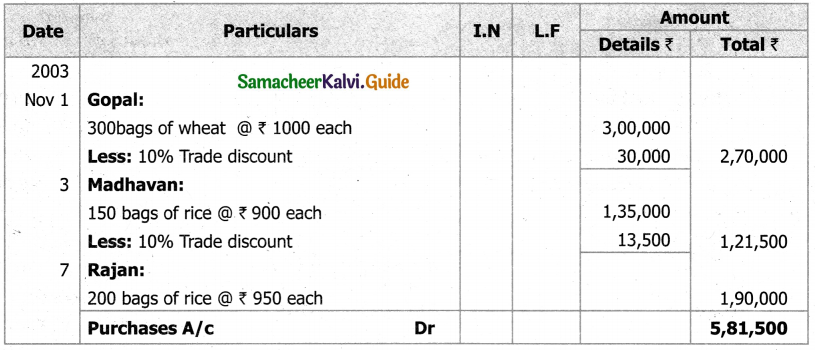

Question 1.

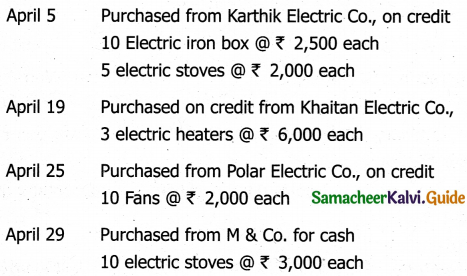

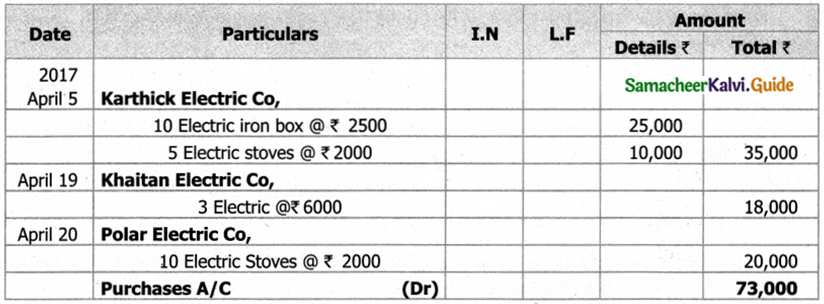

Enter the following transactions in the Purchases book of M/s. Subhashree Electric Co., which deals in electric goods?

Solution:

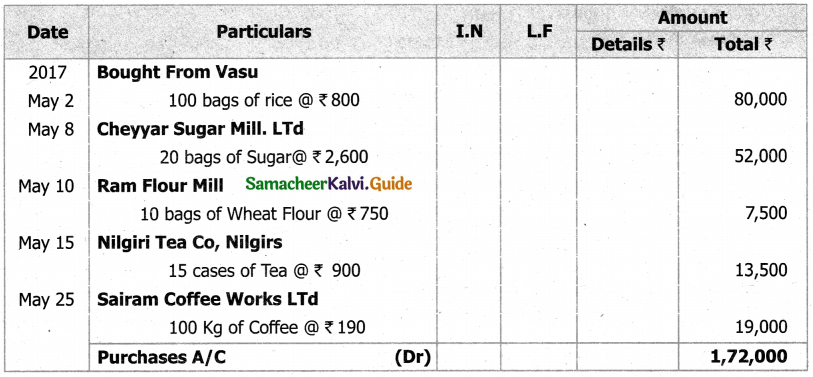

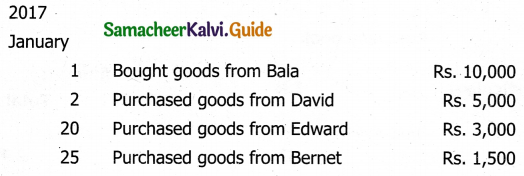

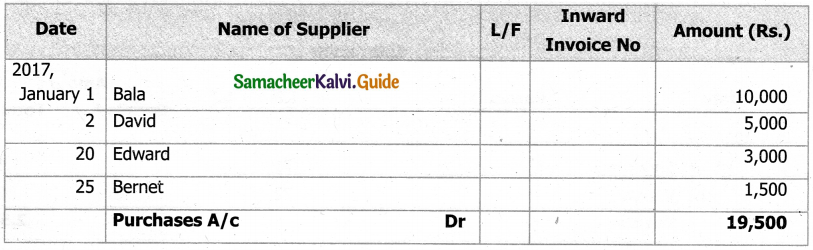

Question 2.

Enter the following credit transactions in the purchases book of Manoharan, a Provisions Merchant.

2017

May 2 – Bought from Vasu 100 bags of rice @ ₹ 800 per bag

May 8 – Bought from Cheyyar Sugar Mills Ltd., 20 bags of sugar @ ₹ 2,600 per bag

May 10 – Bought from Ram Flour Mill, Coimbatore, 10 bags of wheat flour @ ₹ 750 per bag

May 15 – Bought from Nilgiri Tea Co., Nilgiris, 15 cases of tea @ ₹ 900 per case

May 25 – Bought from Sairam Coffee Works Ltd., 100 kgs of Coffee @ ₹ 190 per kg.

May 29 – Bought from X & Co. furniture worth ₹ 2,000

Solution:

In the books of Manoharan Provisional Merchant Purchases as book.

![]()

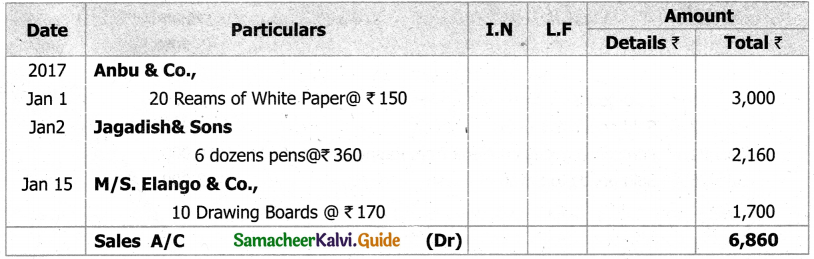

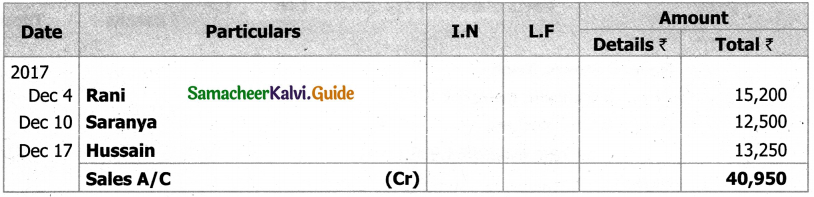

Question 3.

From the following transactions write up the Sales day book of M/s. Ram & Co., a stationery. merchant.

2017

Jan. 1 – Sold to Anbu & Co., on credit 20 reams of white paper @ ₹ 150 per ream

Jan. 2 – Sold to Jagadish & Sons on credit 6 dozen pens @ ₹ 360 per dozen

Jan. 10 – Sold old newspapers for cash @ ₹ 620

Jan. 15 – Sold on credit M/s. Elango & Co., 10 drawing boards @ ₹ 170 per piece

Jan. 20 Sold to Kani & Co., 4 writing tables at ₹ 1,520 per table for cash

Solution:

In the books of M/s. Ram & Co. a Stationary Merchant

Sales Book

Question 4.

Enter the following transactions in the Sales book of Kamala Stores, a furniture shop.

2017

May 2 – Sold to Naveen Stores, Trichy on credit 5 computer tables @ ₹ 1,750 per table

May 9 – Sold to Deepa & Co., Madurai on credit 6 dining tables @ ₹ 1,900 per dining table

May 15 – Sold to Rajesh 10 dressing tables @ ₹ 2,750 each on credit

May 24 – Sold to Anil 5 wooden tables @ ₹ 1,250 per table on credit

May 27 – Sold to Gopi 3 old computers @ ₹ 3,500 each

May 29 – Sold 50 chairs to Anil @ ₹ 275 each for cash

Solution:

In the books of Kamala Stores a Furniture’s Shop

Sales book

Question 5.

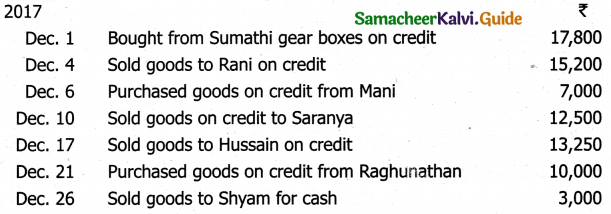

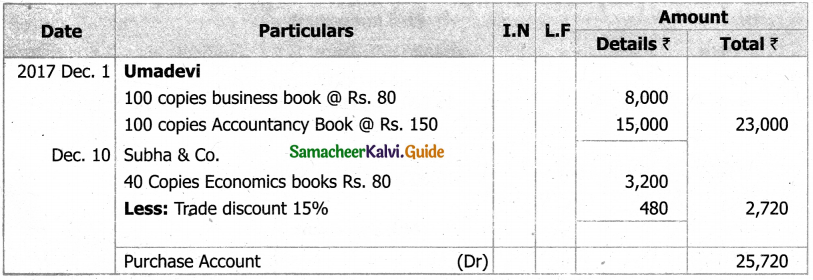

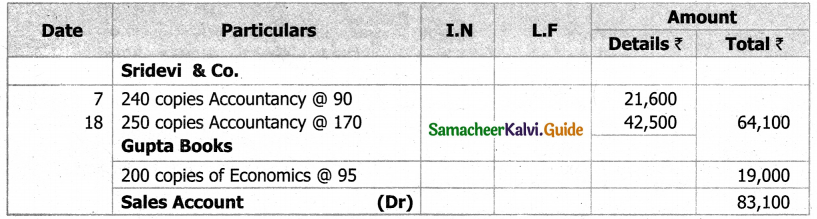

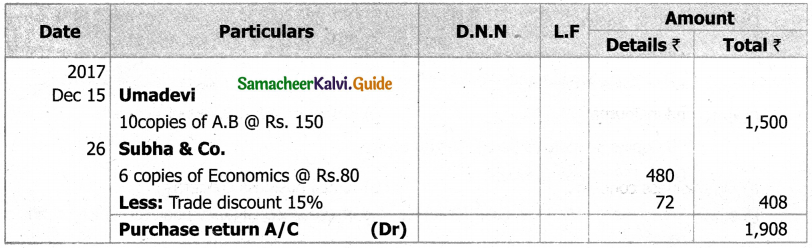

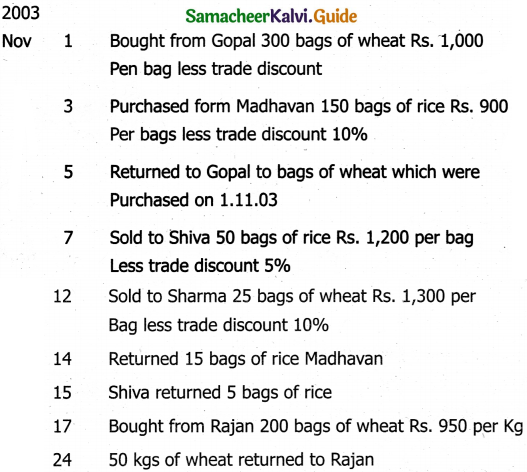

Enter the following transactions in the purchases and sales books of Kannan, an automobile dealer, for the month of December, 2017.

Solution:

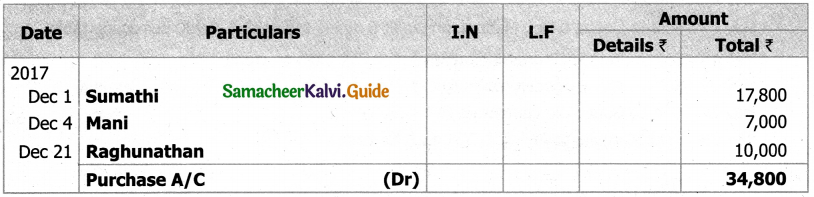

In the books of Kannan

Purchase book

In the books of Kannan

Sales book

Question 6.

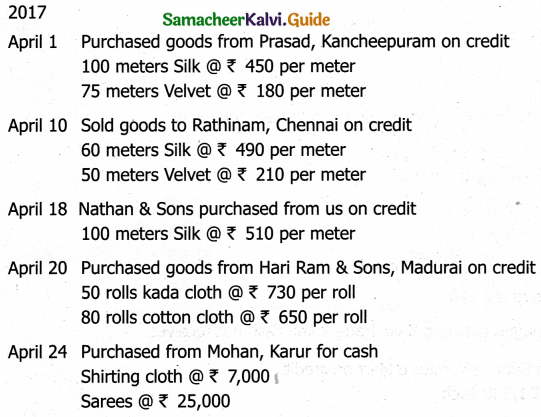

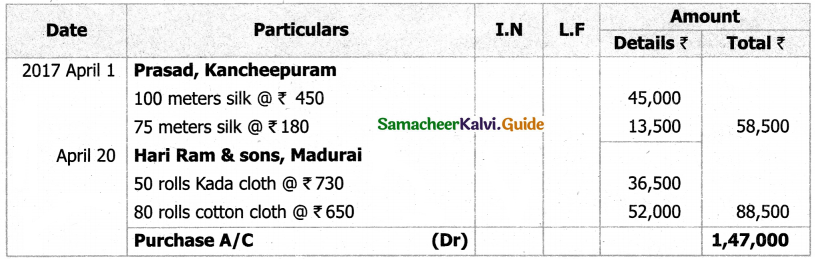

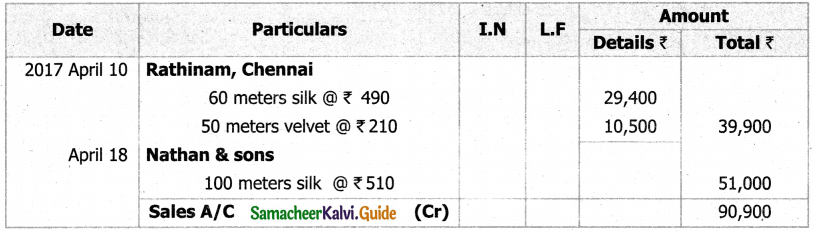

Prepare Purchases book and Sales book in the books of Santhosh Textiles Ltd., from the following transactions given for April, 2017.

Solution:

In the books of Santhosh Textile Ltd,

Purchase Book

In the books of Santhosh Textile Ltd,

Sales Book

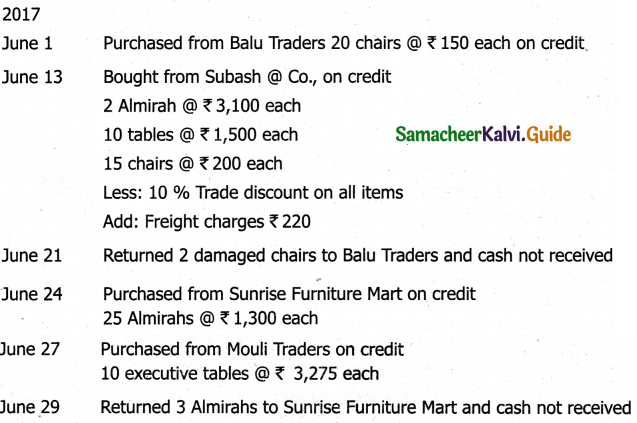

Question 7.

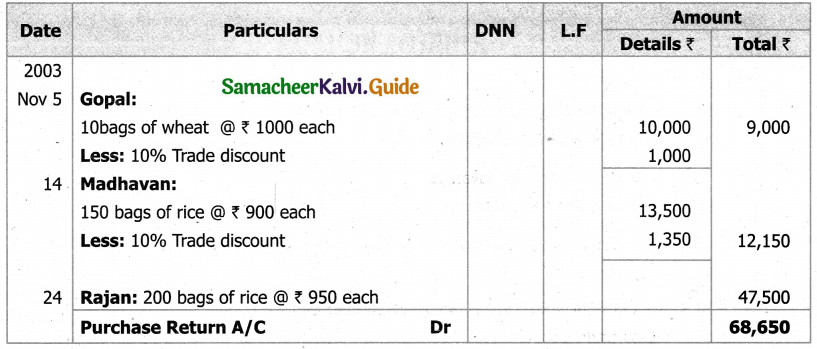

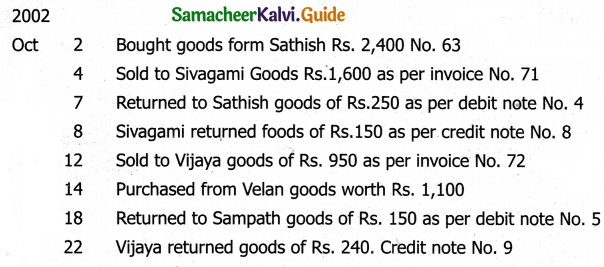

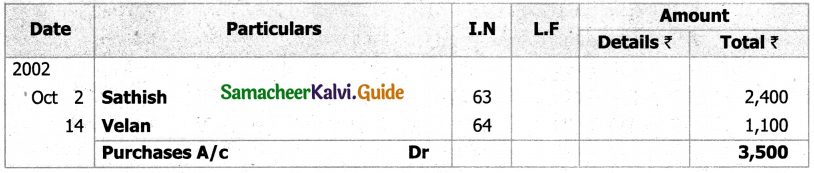

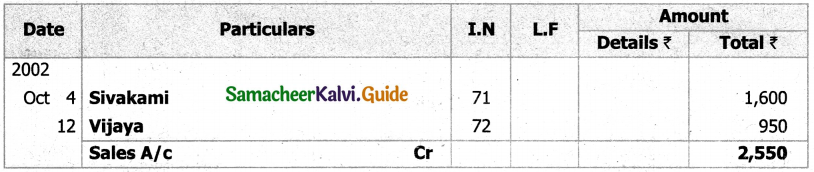

From the following information, prepare purchase day book and purchases returns book for the month of June, 2017 and post them into ledger accounts in the books of Robert Furniture Mart.

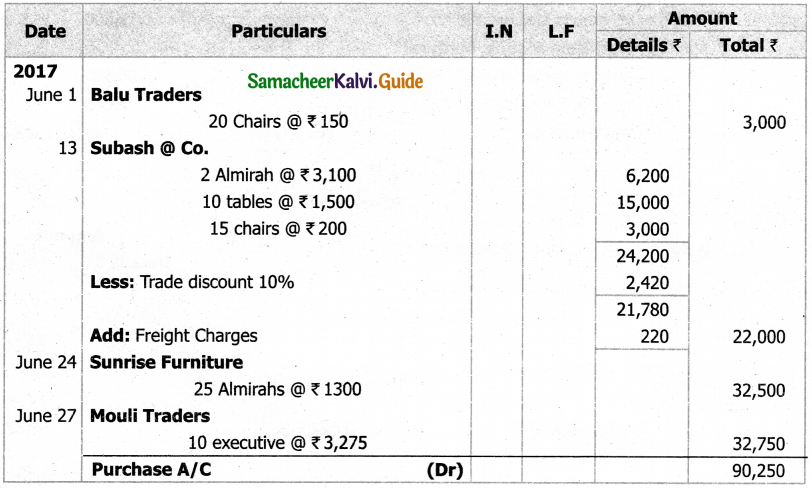

Solution:

In the books of Robert Furniture Mart.

Purchases Book

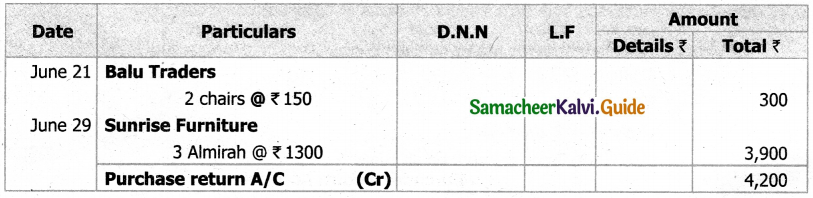

In the books of Robert Furniture Mart.

Purchase return A/C

Ledger Account

Purchases Account

Balu Traders

Subash & Co.

Sunrise Furniture

Mouli Traders

Purchase Return Account

![]()

Question 8.

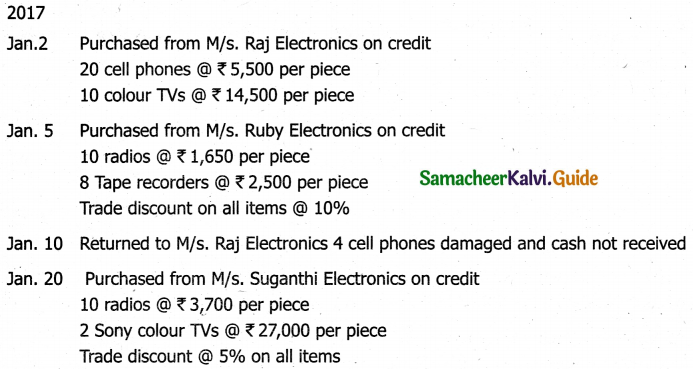

Enter the following transactions in the proper subsidiary books of Suman who is dealing in electronic goods for the month of January, 2017.

Solution:

In the books of Suman

In the books of Suman

Purchase Returns Book

Question 9.

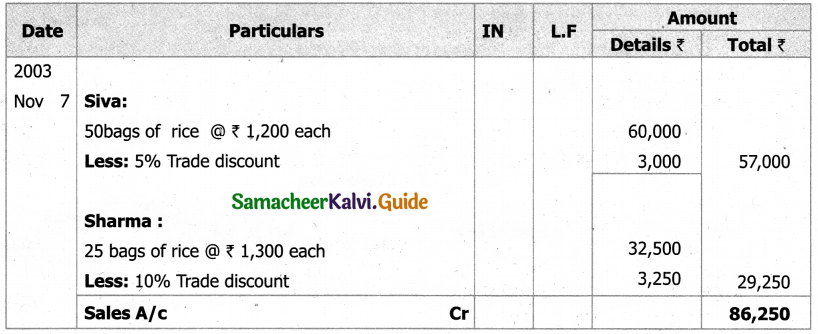

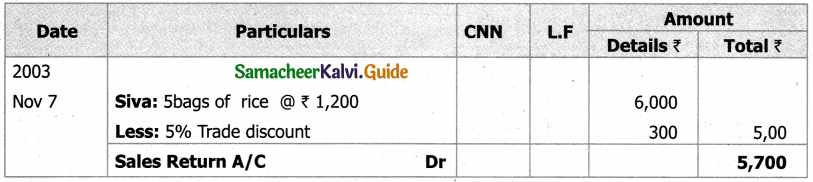

Enter the following transactions in the sales book and saies returns book of M/s. Guhan & Sons, who is a textile dealer.

Solution:

In the books of Guhan & Sons

Sales Books

In the books of Guhan & Sons

Sales Return Book

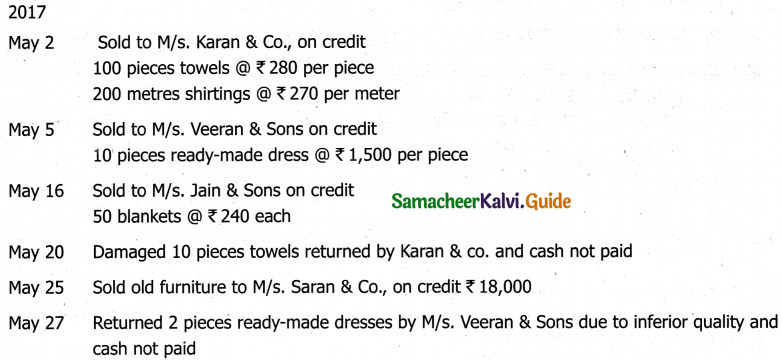

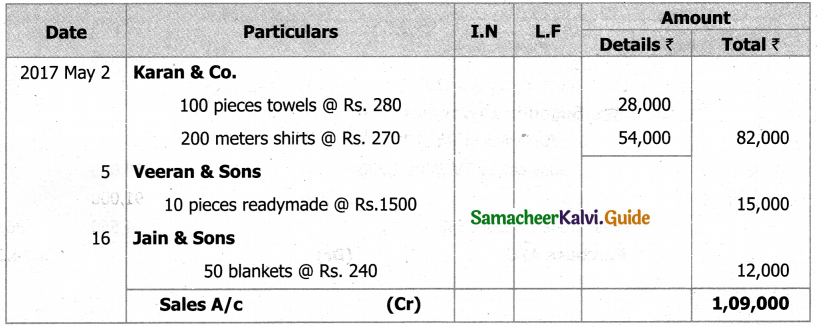

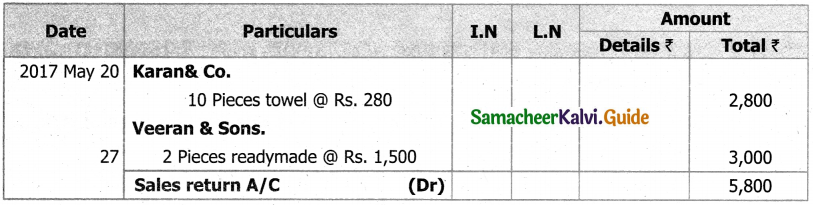

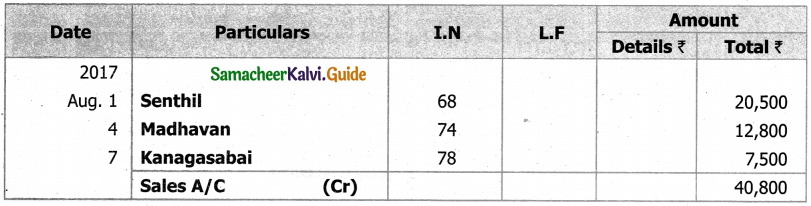

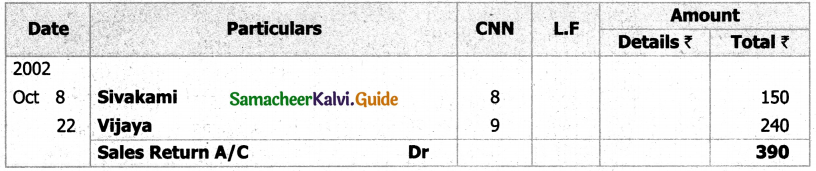

Question 10.

Record the following transactions in the sales book and sales returns book of M/s. Ponni & Co., and post them to ledger.

2017

Aug 1 – Sold goods to Senthii as per Invoice No. 68 for ₹ 20,500 on credit

Aug 4 – Sold goods to Madhavan as per Invoice No. 74 for ₹ 12,800 on credit

Aug 7 – Sold goods to Kanagasabai as per Invoice No. 78 for 17,500 on credit

Aug 15 – Returns inward by Senthii as per Credit Note no. 7 for ₹ 1,500 for which cash is not paid

Aug 20 – Sold goods to Selvarn for ₹ 13,300 for cash

Aug 25 – Sales returns of 11,800 by Madhavan as per Credit Note No. 11 for which cash is not paid

Solution:

In the books of Ponni & Co

Sales Book

In the books of Ponni & Co.

Sales Return Book

Ledger A/C

Sales Account

Senthil Account

Madhavan Account

Kanagasabai Account

Kanagasabai Account

Sales Return Account

Question 11.

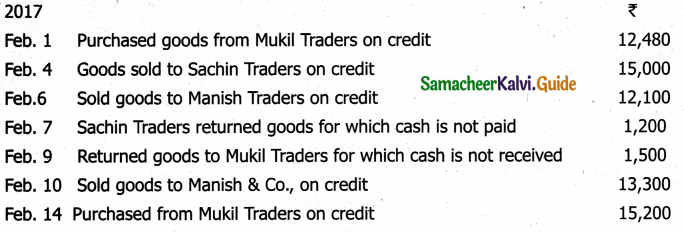

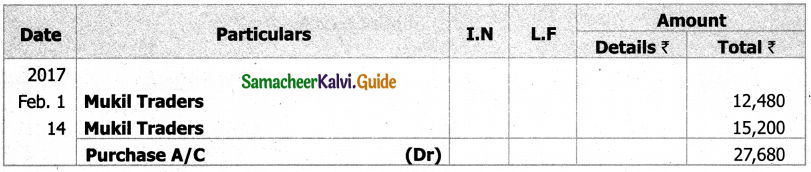

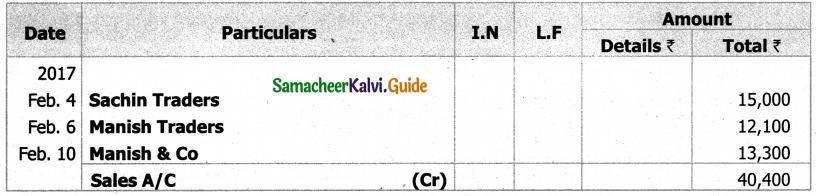

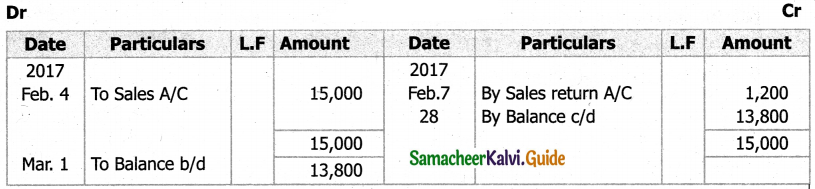

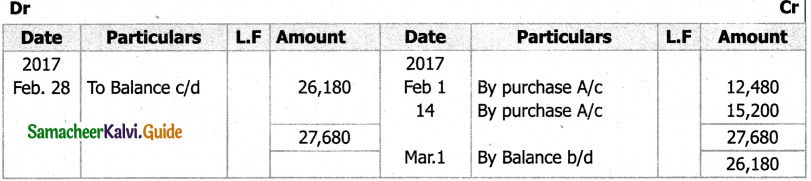

Prepare necessary subsidiary books in the books of Niranjan and aiso Sachin account and Mukil account from the following transactions for the month of February, 2017.

Solution:

In the books of Sachin account and Mukil account.

Purchase Book (Mukil Account)

Sales Book

Purchase Return Book

Sales return Book

Ledger

Sachin Account

Mukil Account

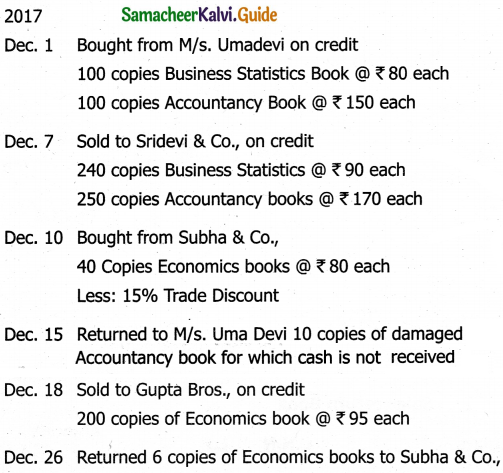

Question 12.

From the following information, prepare the necessary subsidiary books for Nalanda Book Stores.

Solution:

In the books of Naianda Book Stores

Purchase Book

In the books of Naianda Book Stores

Sales Book

Purchase return books

![]()

11th Accountancy Guide Subsidiary Books – I Additional Important Questions and Answers

I. Choose the correct answer

Question 1.

If goods are sold but not delivered to the customer, they will be included in _______.

a) Closing Inventory

b) Goods in transit

c) Sales

d) Sales in returns

Answer:

b) Goods in transit

Question 2.

Goods Of Rs.800 (sales price) sent on sale on approval basis were included In the sales book. The profit included in the sales was 25% on cost. Inventory with the party will increase our closing inventory by _______.

a) Rs. 600

b) Rs. 640

c) Rs. 680

d) Rs. 700

Answer:

b) Rs. 640

Question 3.

List price of the goods purchased is Rs. 60,000 cash paid is Rs. 45,000 (After receiving a cash discount of Rs. 9,000) the trade discount will be?

a) 10 %

b) 7.5 %

c) 15 %

d) 25 %

Answer:

a) 10 %

Question 4.

A trader purchased goods for Rs. 4,000 at a discount of 5%. As he paid the amount immediately, a cash discount of Rs.100 was also allowed. In this case, Purchases A/c is debited by:

a) Rs. 4,000

b) Rs. 3,800

c) Rs. 3,700

d) Rs. 3,900

Answer:

b) Rs. 3,800

![]()

Question 5.

The periodical total of the Sales Return Book is posted to the _______.

a) Debit side of Sales Account

b) Debit side of Sales Return Account

c) Credit side of Sales Return Account

d) Debit side of Debtors Return Account

Answer:

b) Debit side of Sales Return Account

Question 6.

Debit notes issued are used to prepare _______.

a) Sales returns book

b) Puchases returns book

c) Journal proper

d) Puchases book

Answer:

b) Puchases returns book

Question 7.

Trade discount allowed at the time of sale of goods is _______.

a) Recorded in Sales Book

b) Recorded in Cash Book

c) Recorded in Journal

d) Not recorded in Books of Accounts

Answer:

d) Not recorded in Books of Accounts

Question 8.

Subsidiary books are maintained in _______.

a) Big business concerns

b) Small business concerns

c) Banks

d) None of the above

Answer:

a) Big business concerns

Question 9.

Journal Proper is used to record _______.

a) Ail cash and credit transaction

b) cash and credit sales

c) Cash and credit purchases

d) adjusting and closing entries

Answer:

d) adjusting and closing entries

Question 10.

Cash discount is recorded in the _______.

a) Cash book

b) Sales Book

c) Purchases book

d) Journal

Answer:

a) Cash book

Question 11.

The cash discount allowed to a debtor should b e credited to _______.

a) Discount Account

b) Customer’s Account

c) Sales account

d) None of the above

Answer:

b) Customer’s Account

Question 12.

Which of the following books should be used to record purchase of furniture on credit?

a) Petty Cash Book

b) Journal Proper

c) Cash Book

d) None of the above

Answer:

b) Journal Proper

![]()

Question 13.

The return of goods to a supplier should be credited to _______.

a) Supplier Account

b) Goods Account

c) Purchase Return Account

d) None of the above

Answer:

c) Purchase Return Account

Question 14.

The other name of Sales Returns book is _______.

a) Returns Inwards Book

b) Sales Returns Journal

c) both (a) & (b)

d) None of the above

Answer:

c) both (a) & (b)

Question 15.

The statement sent to the suppliers on account of return of goods is known as _______.

a) Debit Note

b) Credit Note

c) Journal Proper

d) None of the above

Answer:

a) Debit Note

Question 16.

On 1st January 2918, pugazh draws a bill on Sundar for 3 months, Its due date is _______.

a) 31st March 2018

b) 1st April 2018

c) 4th April 2018

d) 4th April 2018

Answer:

c) 4th April 2018

Question 17.

Goods returned by customers are recorded in _______.

a) Sales book

b) sales return book

c) Purchases book

d) purchases return book

Answer:

b) sales return book

Question 18.

Goods returned by suppliers are recorded in _______.

a) Sales book

b) sales return book

c) Purchases book

d) purchases return book

Answer:

d) purchases return book

Question 19.

Days of grace are _______ in number.

a) one

b) two

c) three

d) four

Answer:

c) three

Question 20.

The person who prepares a bill is called the _______.

a) Drawer

b) Drawee

c) Payee

d) All of these

Answer:

a) Drawer

Question 21.

The person who has to make the payment or who accepts to make the payment is called _______.

a) Drawer

b) Drawee

c) Payee

d) All of these

Answer:

b) Drawee

![]()

Question 22.

The person who receives the payment is payee _______.

a) Drawer

b) Drawee

c) Payee

d) All of these

Answer:

d) All of these

Question 23.

_______ means signing on the face or back of a bill for the purpose of transferring the title of the bill to another person.

a) Endorsement

b) Discounting

c) Retiring of bill

d) Renewal

Answer:

a) Endorsement

Question 24.

_______ is the statement prepared by the seller of goods.

a) Voucher

b) Receipt

c) Invoice

d) Ledger

Answer:

c) Invoice

Question 25.

Puchases book does not keep record of purchases of _______.

a) Purchases book

b) sales book

c) Purchases returns book

d) sales returns book

Answer:

a) Purchases book

II. Very Short Answer Type Questions

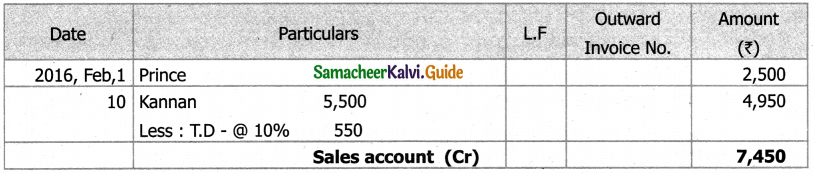

Question 1.

Prepare Sales Book of M/S A :

i. 2016, Feb, 1 – Sold goods to prince Rs. 2,500

i. 2016, Feb 10 – Sold to Kannan 100 shirts @ Rs. 55 per shirt, Trade discount 10%

ii. 2016, Feb 26 – Sold old furniture to Rasi & sons Rs. 2,400 on credit.

Solution:

Sales Book

Question 2.

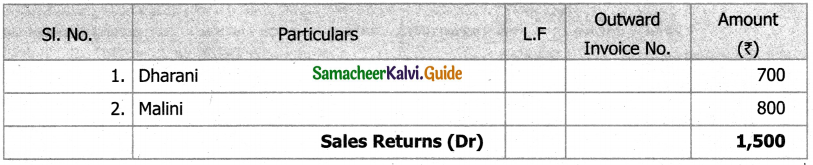

Record the following transactions in the returns inwards book of Mr. A.

1. Dharani returned goods worth Rs. 700

2. Malaini returned goods worth Rs. 800

Answer:

Sales Returns Book

![]()

III. Short Answer Questions

Question 1.

What is trade discount?

Answer:

Trade discount is a deduction given by the supplier to the buyer on the list price or catalogue price of the goods. It is given as a trade practice or when goods are purchased in large quantities. It is shown as a deduction in the invoice. Trade discount is not recorded in the books of accounts. Only the net amount is recorded.

Example : Suppose the sale of goods for ₹ 10,000 was made and 10% was allowed as trade discount, the entry regarding sales will be made for Rs 9,000 (10,000 – 10 per cent of 10,000). In the same way, purchaser of goods will also record purchases as Rs 9,000).

Question 2.

Write notes on parties involved in a bill of exchange.

Answer:

There are three parties to a bill of exchange as under:

- Drawer : The person who prepares the bill is called the drawer, i.e., a creditor.

- Drawee : The person who has to make the payment or who accepts to make the payment is called the drawee, i.e., a debtor.

- Payee : The person who receives the payment is payee. He may be a third party or the drawer of the bill.

Question 3.

What are the features of bills of exchange?

Answer:

- It is a written document.

- It is an unconditional order.

- It is an order to pay a certain sum of money.

- It is signed by the drawer.

- It bears stamp or it is drafted on a stamp paper.

- It is to be accepted by the acceptor.

Question 4.

What is Due date?

Answer:

When a bill is drawn payable after a specified period, the date on which the payment should be made is called ‘Due date’.

Question 5.

What is Days of grace?

Answer:

In the calculation of the due date, three extra days are added to the specified period of the bills called ‘Days of grace’. If the date of maturity falls on a holiday, the bill will be due for payment on the preceding day.

Question 6.

Write notes on retiring of a bill.

Answer:

An acceptor may make the payment of a bill before its due date and may discharge the liability on the bill. It is called as retirement of a bill. Usually, the holder of the bill allows a concession called rebate to the drawee for the unexpired period of the bill.

![]()

Question 7.

Write notes on renewal of a bill of exchange.

Answer:

When the acceptor of a bill knows in advance that he/she will not be able to meet the bill on its due date, he/she may request the drawer for extension of time for payment. The drawer of the bill may agree to cancel the original bill and draw a new bill for the amount due with interest thereon. This is referred to as renewal.

Question 8.

Write notes on closing entries.

Answer:

At the end of the accounting period, all the ledger accounts relating to purchases, sales, purchases returns, sales returns, stock and other accounts concerning expenses, losses, incomes and gains are closed by transfer to trading and profit and loss account so that financial statements can be prepared. It should be noted that closing entries are made for nominal accounts only.

Question 9.

Write notes on rectifying entries.

Answer:

Rectifying entries are passed for rectifying errors which are committed in the books of accounts.

Example : Purchase of furniture by a stationery dealer for Rs 10,000 was debited to purchases account. Pass rectifying entry on December 31, 2017.

Rectifying Entry

Question 10.

What is Endorsement?

Answer:

Endorsement means signing on the face or back of a bill for the purpose of transferring the title of the bill to another person. The person who endorses is called the “Endorser”. The person to whom a bill is endorsed is called the “Endorsee”. The endorsee is entitled to collect the money.

Question 11.

What is discounting?

Answer:

When the holder of a bill is in need of money before the due date of a bill, cash can be received by discounting the bill with the banker. This process is referred to as the discounting of bill. The banker deducts a small amount of the bill which is called discount and pays the balance in cash immediately to the holder of the bill.

Question 12.

State the reasons for returning of the goods?

Answer:

- not according to the order placed.

- not upto the samples which were already shown.

- due to damage condition.

- due to price difference.

- undue delay in the delivery of the goods.

Question 13.

What are the kinds of returns books?

Answer:

- Purchases Return or Returns outward book.

- Sales Return or Returns inward book.

![]()

Question 14.

What is Bills payable book?

Answer:

Details recorded in the bills payable book are the names of the parties whose bills are accepted, date of the bills payable, due date, amount, etc. The individual accounts of the parties whose bills are accepted will be debited with the corresponding amount in the bills payable book.

Question 15.

What is Bills receivable book?

Answer:

Bills receivable refers to bills drawn, the payment for which has to be received. In case of credit sales of goods, the entity may draw a bill on the buyer (debtor), for a certain period. This is called bills receivable for the business entity and bills payable for the debtor who has accepted the bill.

IV. Exercises

Question 1.

From the following transactions of Ram Home appliances for July, 2017 prepare pui books and ledger accounts connected with his book.

Solution:

In the books of ram home appliances

Purchase book

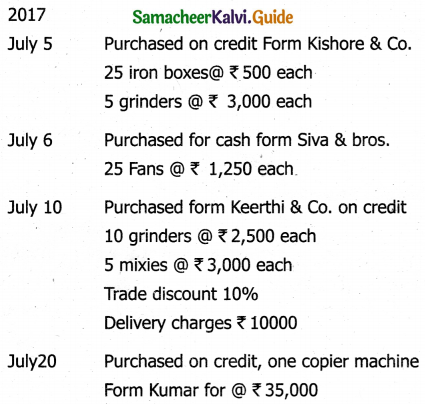

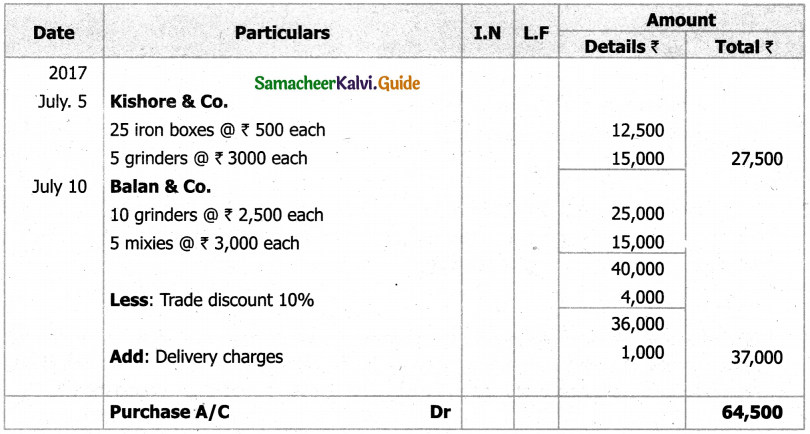

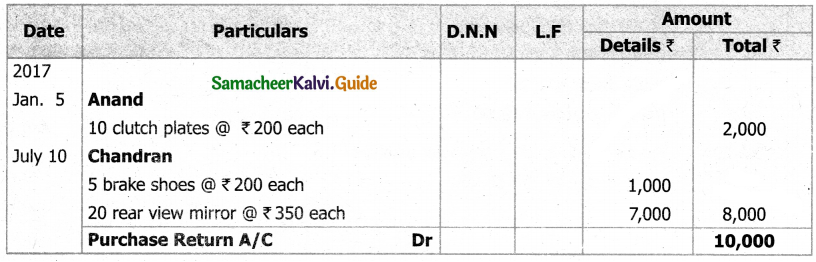

Question 2.

Enter the following transactions in the purchases returns book of Hair who lealing in auto mobiles and post them into the 2017

2017

Jan 5 – Returned to Anand 10 dutch plates @ ₹ 200 each not in accordance with order.

Jan 14 – Returned to Chardran 5 brake shoes @ ₹ 200 each and 20 rear view Mirrors @ ₹ 350, each due to inferior quality

Solution:

In the books of Hari

Purchases Return book

Question 3.

From the transactions given below, Prepare the sales book of Kumar Stationery of July 2017,

Solution:

Sales account

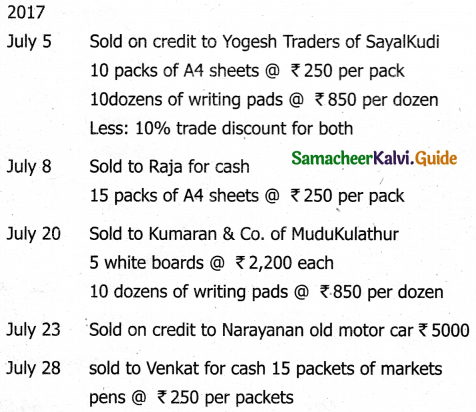

Ledger Accounts

Sales Account

Yogesh Traders A/c

Kumaran & Co, A/c

Question 4.

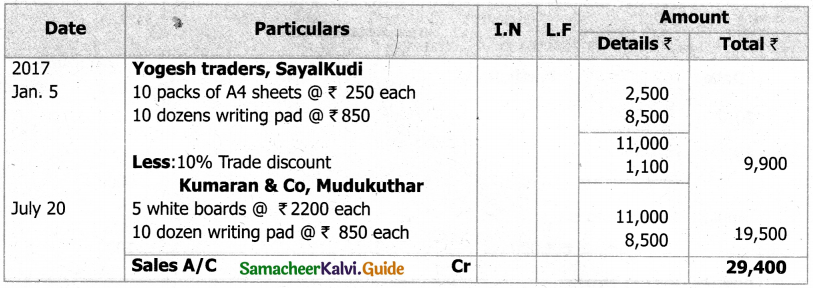

Enter the following transaction in returns inward book of Magesh a textile dealer.

2017

April 6 – Returned by Naren 40 shirts each costing ₹ 150 due top inferior Quality.

April 8 – Amar Tailors returned 10 T-shirts, each costing ₹ 100 on accounts Of being not in accordance with their order.

April 21 – Prema stars returned 20 salwar sets each costing ₹ 200, being not in Accordance with order.

Solution:

In the books of Magesh

Sales Return book

Question 5.

Enter the following transactions in proper subsidiary books.

Solution:

Purchase Book

Sales book

![]()

Question 6.

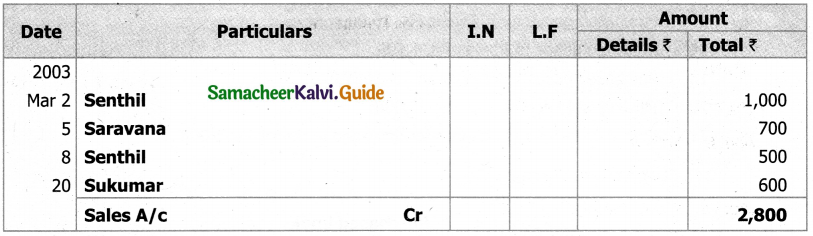

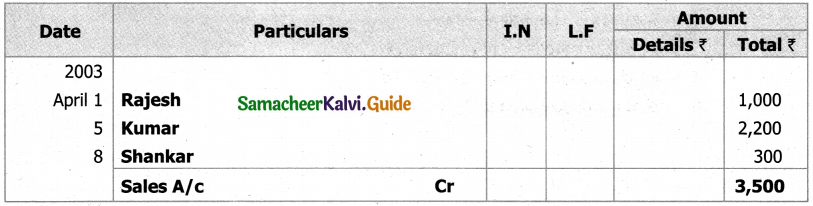

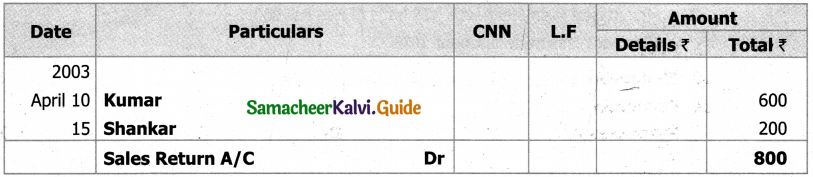

Record the following transaction in the proper subsidiary books of M/S Ram & Co.

April

1 – Goods sold to Ramesh Rs. 1000

3 – Sold goods to Kumar Rs. 2,200.

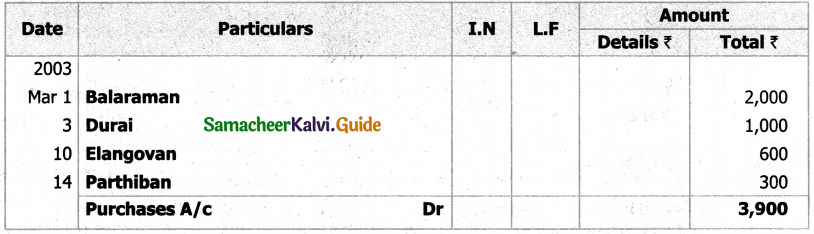

8 – Sold goods to Shankar Rs. 300

10 – Goods returned by Kumar Rs. 600.

15 – Credit note sent to Shankar For Rs. 200

Solution:

In the books of Ram & Co.

Sales book

Sales Return Book

Question 7.

Write the following transaction in proper subsidiary books of Mr. Pugazh.

In the books of Mr. Pugazh

Purchased book

In the books of Mr. Pugazh

Purchased return book

Question 8.

Enter the following transaction in the proper subsidiary books of Mr. Somu.

Solution:

In the books of Mr. Somu

Purchase book

In the books of Mr. Somu

Purchased return book

In the books of Mr. Somu

Sales book

In the books of Mr. Somu

Sales return book

Question 9.

Enter the following transactions in the appropriate special M/s Padmini & Co.

Solution:

In the books of M/S Padmini

Purchase book

In the books of M/S Padmini

Sales book

In the books of M/S Padmini

Purchase return book

In the books of M/S Padmini

Sale return book

Question 10.

Enter the following transactions in the subsidiary books:

Solution:

Purchases Book

Question 11.

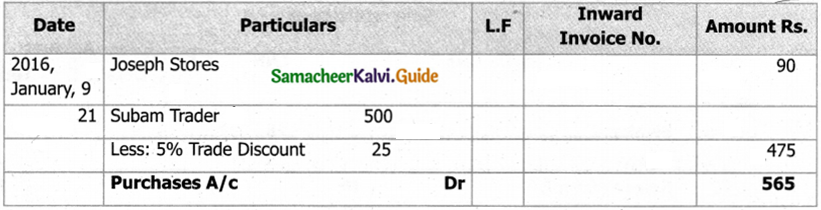

Enter the following transactions in the purchase book of M/S Arun and post them in the ledger:

2016,

Jan.

9 – Purchased from Joseph stores, 15 boxes of pencil @ Rs.6 per box 15 Purchased for cash 10 Exercise book @ Rs.5 per book

18 – Bought Furniture from Fancy Furniture Mart for Rs.2,000, Trade discount @ 10%

21 – Purchased 25 bags of tea dust from Subam Traders @ Rs.20 per bag, Trade discount 5%

Solution:

Purchases Book

![]()

Question 12.

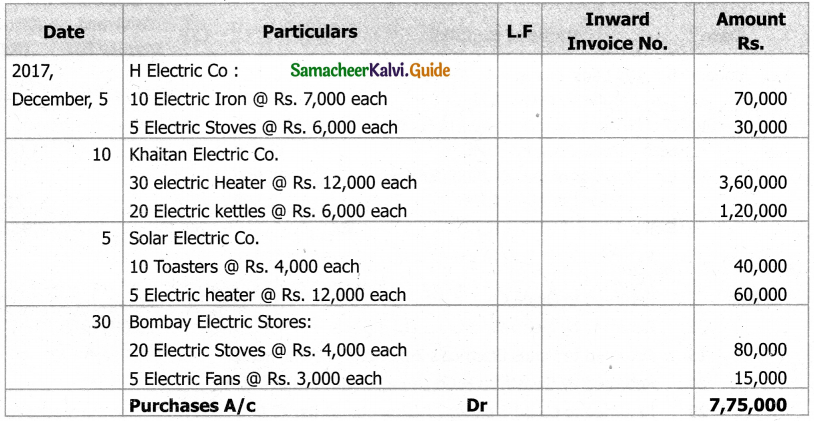

From the particulars given below, write up the Purchases Day Book of M/s Hilton Electric Co, which deals in electrical goods:

2017,

Dec.

5 – Purchased on Credit from H Electric Co. – 10 Electric Iron @ Rs. 7,000 each; 5 – Electric Stoves @ Rs. 6,000 each;

16 – Purchased on credit from Khaitan Electric Co – 30 Electric Heater @ Rs. 12,000 each; 20 Electric Kettles @ Rs. 6,000 each;

21 – Purchased from Solar Electric Co. on credit – 10 Toasters @ Rs. 4,000 each; 5 – Electric Heater @ Rs. 12,000 each;

30 – Purchased from Bombay Electric Stores on Credit – 20 Electric Stoves @ Rs. 4,000 each; Electric Fans @ Rs. 3,000 each;

Solution:

Purchases Day Book

Question 13.

Enter the following transactions in the sales book of Arun and post them into ledger.

2016,

Jan.

1 – Sold goods to Prince Rs. 2500

10 – Sold to Kannan 100 Shirts @ Rs. 45 per shirt, Trade discount 10%

21 – Sold old furniture to Kumar & Sons Rs. 1,200 on credit

Solution:

Sales Day Book

Question 14.

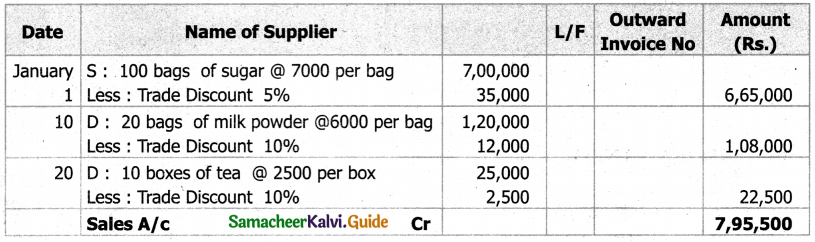

From the following transactions write up the sales day book of M/s Rajesh & Co.

Jan.

1 – Sold to S 100 bags of sugar @ Rs. 7,000 per bag, less trade discount @ 5%

10 – Sold to D 20 bags of milk powder @ Rs. 6,000 per bag, less trade disc. @ 10%

20 – Sold to F 10 boxes of Tea @ Rs. 2,500 per box, less trade discount @ 10%

29 – Sold old office furniture on credit to Rainbow furniture mart for Rs. 64,000

Solution:

Sales Day Book

Question 15.

Enter the following information in the proper subsidiary books:

Mar.

1 – Returned to Onida Co. Ltd 4 colour TVs @ Rs. 24,000 each

2 – Returned by Metro Electronics Ltd 4 pieces of Fridge costing Rs. 20,000 each

15 – Returned to Venus Electricals 2 pieces of electric heater @ Rs. 6,500 each

24 – Returned by Swasthica & Co , 4 pieces of Speakers costing Rs. 9,000 each

29 – Returned to LG ltd 3 pieces of Computer @ Rs. 40,000 each which was purchased for cash.

Solution:

Purchase Returns Book

Sales Return Book

![]()

Question 16.

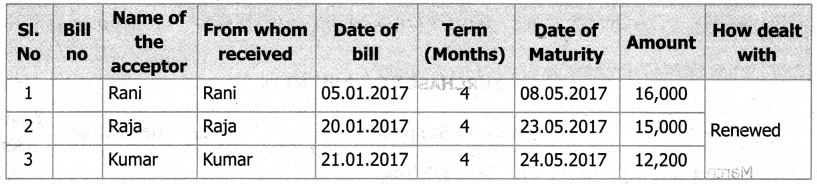

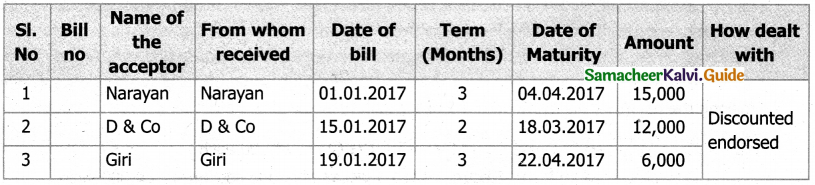

Record the following transactions in the bills receivable and the bills payable books of a trader:

2017

January

1 – Received from Narayan an acceptance of 3 months for Rs. 15,000

5 – Our acceptance to Rani at 4 months for Rs. 16,000

15 – Received from D & Co an acceptance for 2 months for Rs. 12,000

18 – Discount Narayan acceptance for Rs. 9,800

19 – Received from Giri an acceptance for 3 months for Rs. 16,000

20 – Our acceptance to Raja at 4 months for Rs. 15,000

21 – Kumar Renewed our acceptance to Rani by paying him cash Rs. 12,000 and accepted a fresh bill of Rs. 12,200 at 4 months, Rs. 200 has being interest charged

22 – D & Co acceptance endorsed in favour of G in full settlement of a debt of Rs. 2,250

Solution:

Bills Receivable Book

Bills Payable Book