Tamilnadu State Board New Syllabus Samacheer Kalvi 11th Accountancy Guide Pdf Chapter 11 Capital and Revenue Transactions Text Book Back Questions and Answers, Notes.

Tamilnadu Samacheer Kalvi 11th Accountancy Solutions Chapter 11 Capital and Revenue Transactions

11th Accountancy Guide Capital and Revenue Transactions Text Book Back Questions and Answers

![]()

I. Multiple Choice Questions

Choose the correct answer.

Question 1.

Amount spent on increasing the seating capacity in a cinema hall is _______.

a) Capital expenditure

b) Revenue expenditure

c) Deferred revenue expenditure

d) None of the above.

Answer:

a) Capital expenditure

Question 2.

Expenditure incurred ₹ 20,000 for trial run of a newly installed machinery will be _______.

a) Preliminary expense

b) Revenue expenditure

c) Capital expenditure

d) Deferred revenue expenditure

Answer:

c) Capital expenditure

Question 3.

Interest on bank deposits is _______.

a) Capital receipt

b) Revenue receipt

c) Capital expenditures

d) Revenue expenditures

Answer:

b) Revenue receipt

Question 4.

Amount received from IDBI as a medium term loan for augmenting working capital _______.

a) Capital expenditures

b) Revenue expenditures

c) Revenue receipts

d) Capital receipt

Answer:

d) Capital receipt

![]()

Question 5.

Revenue expenditure is intended to benefit _______.

a) Past period

b) Future period

c) Current period

d) Any period

Answer:

c) Current period

Question 6.

Pre – operative expenses are _______.

a) Revenue expenditure

b) Prepaid revenue expenditure

c) Deferred revenue expenditure

d) Capital expenditure

Answer:

d) Capital expenditure

![]()

II. Very Short Answer Type Question

Question 1.

What is meant by revenue Expenditure?

Answer:

- The expenditure incurred for day to day running of the business or for maintaining the earning capacity of the business is known as revenue expenditure.

- It is recurring in nature. It is incurred to generate revenue for a particular accounting period. The revenue expenditure may be incurred in relation with revenue or in relation with a particular accounting period.

- For example, cost of purchases is a revenue expenditure related to sales revenue. Rent and salaries are related to a particular accounting period.

Question 2.

What is capital expenditure?

Answer:

- It is an expenditure incurred during an accounting period, the benefits of which will be available for more than one accounting period.

- It includes any expenditure resulting in the acquisition of any fixed asset or contributes to the revenue earning capacity of the business. It is non- recurring in nature.

Question 3.

What is capital profit?

Answer:

Capital profit is the profit which arises not from the normal course of the business. Profit on sale of fixed asset is an example for capital profit.

Question 4.

Write a short note on revenue receipt.

Answer:

Receipts which are obtained in the normal course of business are called revenue receipts. It is recurring in nature. The amount received is generally small.

Examples:

- Proceeds from sale of goods

- Interest on investments received

- Respet Received

- Dividend from investment in shares.

Question 5.

What is meant by deferred revenue expenditure?

Answer:

- An expenditure, which is revenue expenditure in nature, the benefit of which is to be derived over a subsequent period or periods is known as deferred revenue expenditure.

- The benefit usually accrues for a period of two or more years. It is for the time being, deferred from being charged against income. It is charged against income over a period of certain years.

![]()

III. Short Answer Questions

Question 1.

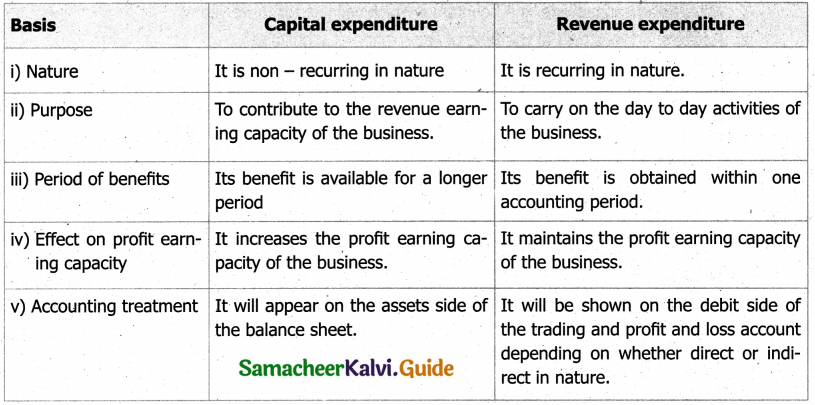

Distinguish between capital expenditure and revenue expenditure.

Answer:

Question 2.

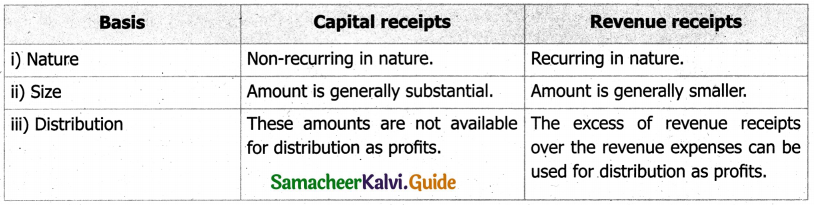

Distinguish between capital receipt and revenue receipt.

Answer:

Question 3.

What is deferred revenue expenditure? Give two examples.

Answer:

1. An expenditure, which is revenue expenditure in nature, the benefit of which is to be derived over a subsequent period or periods is known as deferred revenue expenditure.

2. The benefit usually accrues for a period of two or more years. It is for the time being, deferred from being charged against income. It is charged against income over a period of certain years.

Examples:

- Considerable amount spent on advertising

- Major repairs to plant and machinery

![]()

IV. Exercises

Question 1.

State whether the following expenditures are capital, revenue or deferred revenue.

- Advertising expenditure, the benefits of which will last for three years.

- Registration fees paid at the time of registration of a building.

- Expenditure incurred on repairs and whitewashing at the time of purchase of an old building in order to make it usable.

Solution:

- Deferred revenue expenditure

- Capital Expenditure

- Capital Expenditure

Question 2.

Classify the following items into capital and revenue.

- Registration expenses incurred for the purchase of land.

- Repairing charges paid for remodeling the old building purchased.

- Carriage paid on goods purchased.

- Legal expenses paid for raising of loans

Solution:

- Capital

- Capital

- Revenue

- Capital

Question 3.

State whether they are capital and revenue.

Answer:

- Construction of building ₹ 10,00,000.

- Repairs to furniture ₹ 50,000.

- White-washing the building ₹ 80,000

- Pulling down the old building and rebuilding ₹ 4,00,000

Solution:

- Capital

- Revenue

- Revenue

- Capital

Question 4.

Classify the following items into capital and revenue.

- ₹ 50,000 spent for railway siding.

- Loss on sale of old furniture

- Carriage paid on goods sold.

Solution:

- Capital

- Revenue

- Revenue

Question 5.

State whether the following are capital, revenue and deferred revenue.

- Legal fees paid to the lawyer for acquiring a land ₹ 20,000.

- Heavy advertising cost of ₹ 12,00,000 spent on introducing a new product.

- Renewal of factory licence ₹ 12,000.

- A sum of ₹ 4,000 was spent on painting the factory.

Solution:

- Capital

- Deferred Revenue

- Revenue

- Revenue

![]()

Question 6.

Classify the following receipts into capital and revenue.

- Sale proceeds of goods ₹ 75,000.

- Loan borrowed from bank ₹ 2,50,000

- Sale of investment ₹ 1,20,000.

- Commission received ₹ 30,000.

- ₹ 1,400 wages paid in connection with the erection of new machinery.

Solution:

- Revenue

- Capital

- Capital

- Revenue

- Capital

Question 7.

Identify the following items into capital or revenue.

- Audit fees paid ₹ 10,000.

- Labour welfare expenses ₹ 5,000.

- ₹ 2,000 paid for servicing the company vehicle.

- Repair to furniture purchased second hand ₹ 3,000.

- Rent paid for the factory ₹ 12,000

Solution:

- Revenue

- Revenue

- Revenue

- Capital

- Revenue

![]()

11th Accountancy Guide Capital and Revenue Transactions Additional Important Questions and Answers

I. Choose the correct answer.

Question 1.

Expenses on research and development will be classified under _______.

a) Preliminary expense

b) Revenue expenditure

c) Capital expenditure

d) Deferred revenue expenditure

Answer:

d) Deferred revenue expenditure

Question 2.

Depreciation on fixed asset is a _______ expenditure.

a) Capital expenditure

b) Revenue expenditure

c) Deferred revenue expenditure

d) None of the above.

Answer:

b) Revenue expenditure

Question 3.

Revenue receipts are _______ in the business.

a) non-recurring

b) recurring

c) neither of the above

d) A AND B

Answer:

b) recurring

Question 4.

An plant worth ₹ 8,000 is sold for ₹ 8,500 the capital receipt amounts to _______.

a) ₹ 8,000

b) ₹ 8,500

c) ₹ 500

d) ₹ 165

Answer:

c) ₹ 500

Question 5.

An asset worth ₹ 1,00,000 is sold for ₹ 85,000 the capital loss amounts to _______.

a) ₹ 85,000

b) ₹ 1,00,000

c) ₹ 15,000

d) ₹ 70000

Answer:

c) ₹ 15,000

Question 6.

An asset worth ₹ 1,00,000 is sold for ₹ 75,000 the capital loss amounts to

a) ₹ 1,75,000

b) ₹ 1,00,000

c) ₹ 75,000

d) ₹ 25,000

Answer:

c) ₹ 75,000

![]()

Question 7.

Transaction which provide benefit to*the business for more than one year is called as _______.

a) Capital expenditure

b) Revenue expenditure

c) Deferred revenue expenditure

d) None of the above

Answer:

c) Deferred revenue expenditure

Question 8.

Revenue expenditure is intended to benefit.

a) Subsequent year

b) previous’ year

c) current year

d) None of the above

Answer:

c) current year

II. Very Short Answer Type Questions

Question 1.

What is revenue loss?

Answer:

Revenue losses are the losses that arise from the normal course of the business. In other words, ‘net loss’ – i.e., excess of revenue expenditures over revenue receipts.

Question 2.

Write a short note on Capital receipt.

Answer:

Receipt which is not revenue in nature is called capital receipt. It is non-recurring in nature. The amount received is normally substantial. It is shown on the liabilities side of the balance sheet.

Question 3.

Write the Features of capital expenditure?

Answer:

- It gives benefit for more than one accounting period.

- It includes acquisition of fixed assets and all expenditure incurred upto the point an asset is ready for use.

- It contributes to the revenue earning capacity of the business.

- It is non-recurring in nature.

- It is shown on the assets side of the balance sheet.

Question 4.

Write the Features of revenue expenditure?

Answer:

- It is recurring in nature.

- It is incurred for maintaining the earning capacity of the business.

- Its benefit expires in the same accounting period.

- It is shown on the debit side of the trading and profit and loss account.

Question 5.

Write the Features of deferred revenue expenditure?

Answer:

- It is a revenue expenditure, the benefit of which is to be derived over a subsequent period or periods.

- It is not fully written off in the year of actual expenditure. It is written off over a period of certain years.

- The balance available after writing off (i.e., Actual expenditure – Amount written off) is shown on the assets side balance sheet.

![]()

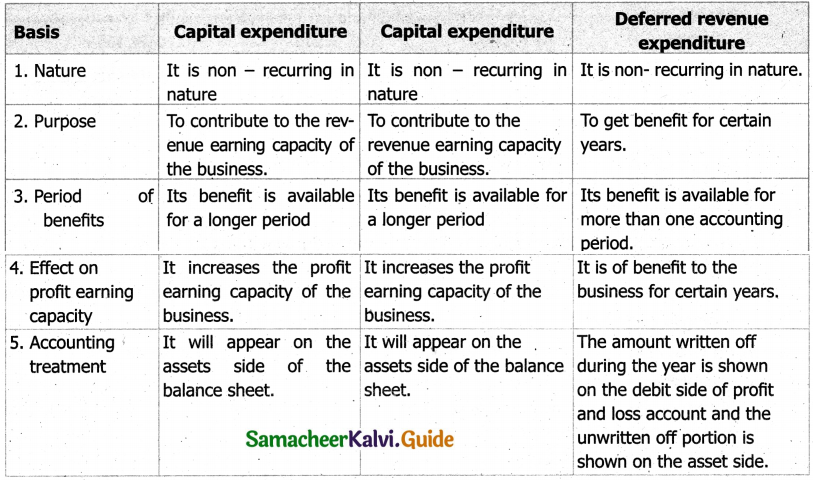

Question 6.

Distinguish Capital, Revenue 8i Deferred revenue expenditure.

Answer:

III. Short Answer Questions

Question 1.

Classify the following expenditures and receipts as capital or revenue

- ₹ 10,000 spent as travelling expenses of the directors on trips abroad for the purchase of fixed assets.

- Amount received from trade receivables during the year.

- Amount spent on demolition of building to construct a large building on the same site.

- Insurance claim received on account of machinery damaged by fire.

Solution:

- Capital expenditure

- Revenue receipt

- Capital expenditure

- Capital receipt.

Question 2.

Classify the following expenses as capital or revenue.

(i) The sum of ₹ 3,200 has been spent on a machine as follows:

- ₹ 2,000 for additions to double the output.

- ₹ 1,200 for repairs necessitated by negligence.

(ii) Overhauling expenses of ₹ 25,000 for the engine of a motor car to get better fuel efficiency.

Solution:

(i) a. capital expenditure

b. revenue expenditure

(ii) capital expenditure.

Question 3.

State whether the following are capital or revenue items.

- ₹ 5,000 spent towards additions to buildings.

- Second-hand motor car purchased for ₹ 30,000 and paid ₹ 2,000 as repairs immediately.

- ₹ 10,000 was spent on painting the new factory.

- Freight and cartage on the new machine ₹ 150, erection charges ₹ 200.

- ₹ 150 spent on repairs before using a second hand car purchased recently.

Solution:

- Capital expenditure.

- Capital expenditure.

- Capital expenditure.

- Capital expenditures.

- Capital expenditure.

Question 4.

State whether the following are capital, revenue or deferred revenue expenditure.

- Carriage of ₹ 1,000 spent on machinery purchased and installed.

- Office rent paid ₹ 2,000.

- Wages of ₹ 5,000 paid to machine operators.

- Hire charges for the use of motor vehicle, hired for five years, but paid yearly.

Solution:

- Capital expenditure.

- Revenue expenditure.

- Revenue expenditure.

- Revenue expenditure.

Question 5.

State with reasons whether the following are capital or revenue expenditure

- Expenses incurred in connection with obtaining a licence for starting the factory for ₹ 25,000.

- A factory shed was constructed at a cost of ₹ 2,00,000. A sum of ₹ 10,000 had been incurred in the construction of temporary huts for storing building material.

- Overhaul expenses of second-hand machinery purchased amounted to ₹ 5,000.

Solution:

- Capital expenditure.

- Capital expenditure.

- Capital expenditure.

![]()

Question 6.

State with reasons whether the following are capital or revenue or deferred revenue expenditure

- Advertisement expenses amounted to ₹ 10 crores to introduce a new product.

- Expenses on freight for purchasing new machinery.

- Freight and insurance on the new machinery and cartage paid to bring the new machinery to the factory.

Solution:

- Deferred revenue expenditure.

- Capital expenditure.

- Capital expenditure.